In a year marked by gradually falling interest rates and economic uncertainty, managing your personal finances has never been more important. Whether you are among the 51% of Americans living paycheck to paycheck or looking to optimize your wealth-building strategy, this guide will show you exactly how to take control of your financial future in 2026.

The Current Financial Landscape: What You Need to Know

Understanding Today’s Economic Reality

The financial environment of 2026 presents both real challenges and genuine opportunities. With the Federal Reserve having cut rates by 75 basis points in 2025 — bringing rates to 3.5% to 3.75% — we are entering a period of transition that informed investors can use to their advantage.

The Congressional Budget Office forecasts inflation will reach 2.4% in 2026, down from 3.1% in 2025, offering some relief to households managing rising costs. However, prices have climbed around 25% since 2020, meaning your dollar still does not stretch as far as it once did. Understanding this environment is the starting point for every financial decision you make this year.

Strategy 1: Master the Art of High-Yield Savings

With rates on savings accounts, CDs, and money market funds typically falling after Fed cuts, right now is the time to lock in today’s best rates before they decline further.

Immediate Steps:

- Open a high-yield savings account offering 4.5% or higher APY — the difference between this and a standard 0.5% account is dramatic over five years.

- Consider laddering CDs to capture current rates before they drop.

- Automate your savings so the decision is made once, not every month.

Pro Tip: Automation is accelerating across personal finance. Tools that automatically move money into savings without manual intervention are no longer optional — they are how consistent savers stay consistent.

Strategy 2: Strategic Debt Elimination

Paying down debt is the most common financial goal for 2026, cited by 19% of Americans — and for good reason. With credit card APRs averaging around 20% and 46% of cardholders carrying balances, debt reduction is not optional. It is urgent.

The Debt Avalanche Method:

- List all debts from highest to lowest interest rate.

- Pay minimums on all debts without exception.

- Attack the highest-rate debt with every extra dollar you can find.

- Once it’s gone, roll that payment into the next debt on the list.

Alternative: The Debt Snowball

- Start with the smallest balance instead of the highest rate.

- Build momentum through quick wins that keep you motivated.

- Works better for people who need psychological reinforcement to stay on track.

Both methods work. The best one is the one you will actually stick to.

Strategy 3: Build Your Emergency Fund Foundation

52% of US adults worry about finances daily. 34% lose sleep over money. An emergency fund is not a nice-to-have — it is the foundation that prevents one unexpected bill from destroying everything else you have built.

Emergency Fund Targets:

- Starter Goal: $1,000 — achievable within 3 to 6 months for most people.

- Standard Goal: 3 to 6 months of total living expenses.

- Advanced Goal: 9 to 12 months for high earners or anyone in an unstable industry.

Quick Win Strategy:

- Sell unused items online — most households have hundreds of dollars sitting in things they no longer use.

- Take on a temporary side gig for 60 to 90 days specifically to fund this account.

- Redirect your next tax refund directly into savings before it hits your regular account.

Strategy 4: Smart Investing for Long-Term Growth

Despite market uncertainty, 79% of Americans are optimistic about their financial future and 63% are hopeful they will reach their financial goals. That optimism needs a strategy behind it.

Beginner Portfolio Allocation by Age:

- Age 20-30: 80% stocks, 20% bonds

- Age 30-40: 70% stocks, 30% bonds

- Age 40-50: 60% stocks, 40% bonds

- Age 50+: 50% stocks, 50% bonds

Investment Vehicles Worth Considering:

- 401(k) or 403(b): Always maximize the employer match first — it is the only guaranteed 100% return you will ever find.

- Roth IRA: Tax-free growth for retirement. One of the most powerful long-term tools available to individual investors.

- Index Funds: Low-cost, diversified, and consistently outperform most actively managed funds over the long run.

- Target-Date Funds: Set your retirement year, let the fund adjust automatically. Simple, effective, and underused.

Strategy 5: Leverage Technology and AI for Financial Success

Conversational AI, embedded finance, and biometric security are becoming standard features in 2026, fundamentally changing how people manage their money day to day.

Must-Have Financial Tools:

- Budgeting Apps: Mint, YNAB, or PocketGuard — pick one and use it consistently.

- Investment Platforms: Fidelity, Vanguard, or robo-advisors for hands-off portfolio management.

- Credit Monitoring: Free services through Experian or Credit Karma. No excuse not to know your score.

- Automated Savings: Apps that round up purchases and save the difference — small amounts that compound into real money over time.

Navigating 2026’s Financial Opportunities

Housing Market Insights

The 30-year fixed mortgage rate is expected to stay above 6% through most of 2026, with Fannie Mae predicting a potential drop to 5.9% only in Q4. Here is how to navigate it depending on your situation:

If You Are Buying:

- Get pre-approved now to understand your real budget before you start looking.

- Consider adjustable-rate mortgages if you plan to move within 5 to 7 years.

- Negotiate seller concessions in a cooling market — more sellers are willing to cover closing costs than they were two years ago.

If You Already Own:

- Avoid refinancing unless rates drop more than 1% below your current rate.

- Consider a HELOC for home improvements — typically lower rates than personal loans.

Side Hustle Economy

Getting a higher-paying job or an additional income source is the second most common financial goal of 2026. The most practical options right now:

- Digital Services: Content creation, virtual assistance, online tutoring — all scalable with low startup costs.

- Gig Economy: Food delivery and rideshare for immediate, flexible income.

- E-commerce: Print-on-demand, dropshipping, or digital products for passive income potential.

- Freelancing: Use your existing professional skills for contract work — the fastest path to meaningful extra income.

Advanced Strategies for Financial Growth

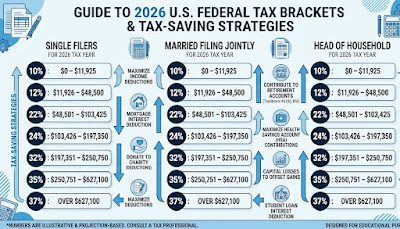

Tax Optimization Techniques

With new charitable giving requirements now requiring contributions to exceed 0.5% of AGI before becoming deductible, tax planning in 2026 requires more deliberate strategy than in previous years.

Key Tax-Saving Moves:

- Maximize retirement contributions to reduce your taxable income directly.

- Use Health Savings Accounts as triple-tax-advantaged vehicles — contributions are deductible, growth is tax-free, and withdrawals for medical expenses are also tax-free.

- Harvest tax losses in investment accounts to offset gains.

- Bundle charitable donations in high-income years to clear the deduction threshold.

Building Multiple Income Streams

Real financial security in 2026 means not depending on a single source of income:

- Dividend-paying stocks and REITs for regular passive income.

- High-yield savings and bond ladders for stable, predictable returns.

- Rental property or REIT exposure for real estate without direct ownership headaches.

- Digital products — courses, ebooks, templates — for income that works while you sleep.

Common Financial Mistakes to Avoid in 2026

- Ignoring Inflation: Even at 2.4%, inflation erodes your purchasing power every single year. Your savings need to outpace it.

- Lifestyle Creep: Spending increases automatically as income grows — unless you consciously redirect those increases into savings and investments first.

- No Financial Plan: 56% of married couples never had a serious money conversation before marriage. Avoiding the subject does not make it simpler.

- Inadequate Insurance: Skimping on health, disability, or life insurance is a false economy. One major event without coverage can eliminate years of progress.

- Emotional Investing: Panic selling during market downturns locks in losses and misses the recovery. This is where most individual investors lose money they did not have to lose.

Your 90-Day Financial Action Plan

Month 1: Foundation Building

- Week 1-2: Track every expense without judgment. Build a realistic budget from what you find.

- Week 3: Open a high-yield savings account and automate transfers from your paycheck.

- Week 4: Review all recurring subscriptions and cut anything you have not used in 30 days.

Month 2: Debt and Credit Optimization

- Week 1-2: Build your debt elimination plan using the Avalanche or Snowball method.

- Week 3: Pull your credit reports, review them, and dispute any errors you find.

- Week 4: Call your credit card companies and negotiate lower rates on existing balances.

Month 3: Growth and Protection

- Week 1-2: Increase retirement contributions by at least 1% — you will not notice it in your paycheck.

- Week 3: Research and implement a simple, low-cost investment strategy suited to your timeline.

- Week 4: Review your insurance coverage and update your beneficiaries on all accounts.

Financial Trends to Watch in 2026

The Rise of Financial Transparency

“Loud budgeting” is becoming mainstream — people are openly sharing financial wins, setbacks, and strategies, breaking down the long-standing stigma around discussing money. This cultural shift makes it easier to find accountability partners, learn from others’ real experiences, and access honest financial education outside of formal institutions.

Technology Integration

The financial tools available in 2026 are fundamentally different from five years ago:

- AI-powered budgeting assistants that learn your spending patterns and flag anomalies.

- Automated investment rebalancing that keeps your portfolio aligned without manual intervention.

- Real-time spending alerts that stop lifestyle creep before it starts.

- Predictive financial planning tools that model multiple scenarios based on your current trajectory.

Conclusion: Your Financial Future Starts Today

Building wealth in 2026 is not about making perfect decisions. It is about making consistent progress — week after week, month after month, regardless of what the market is doing.

55% of Americans plan to save more money this year. 79% are optimistic about their financial future. The strategies in this guide are not complicated. They require discipline, not genius. Start with one thing this week and build from there.

Your Next Steps:

- Choose one strategy from this guide and implement it before the week is out.

- Set up automatic transfers to savings — remove the decision from your hands.

- Schedule a monthly financial check-in with yourself or a partner.

- Track your progress and recognize the wins, however small.

The path to financial freedom is not always comfortable. But with the right knowledge and consistent action, 2026 can be the year your financial trajectory genuinely changes. Start small. Stay consistent. Let time do the heavy lifting.

Disclaimer: This article provides general financial education and should not replace professional financial advice. Consider consulting with a certified financial planner for personalized guidance based on your specific situation.