Key Takeaways

- The 50/30/20 rule was never meant to be a rigid formula — it’s a starting framework, not a law of physics.

- For a growing number of people, needs alone now eat well past 50% of take-home income, especially in high cost-of-living areas.

- The rule still works as a diagnostic tool even when the exact percentages don’t fit your paycheck.

- Adjusting the ratios honestly beats abandoning the framework entirely.

- The “wants” category is where budgets quietly die — not because people are irresponsible, but because nobody defines what actually counts as a want.

- A budget that survives contact with real life matters more than one that looks perfect on paper.

I’ve sat across from more than one person who followed the 50/30/20 rule to the letter, felt proud of the discipline, and still ended every month wondering where the money actually went. The rule wasn’t broken. Their assumptions about what “50% for needs” meant in their specific life were.

The 50/30/20 rule — 50% of take-home pay toward needs, 30% toward wants, 20% toward savings and debt repayment — is one of the most repeated pieces of personal finance advice out there. The question worth actually answering isn’t whether it’s a good rule. It’s whether it holds up once real rent, real groceries, and real life get involved.

What the Rule Was Actually Designed to Do

The framework exists to solve one specific problem: most people have no idea where their money goes until it’s already gone. A budget built around three broad personal budget buckets forces a decision at the start of the month instead of a scramble at the end of it. That’s the actual value — not the specific 50, 30, or 20 numbers themselves.

Treating the percentages as sacred is where people get into trouble. The rule is a starting ratio meant to be adjusted to your actual cost structure, not a fixed target you force your life to match regardless of what it costs to simply exist where you live.

“A budget rule that ignores your actual rent isn’t discipline. It’s denial with a spreadsheet.”

Why “Needs” Has Quietly Grown Past 50% for Many People

Here’s the honest problem nobody addresses directly: cost of living in a lot of places has outpaced the neat 50% assumption. Housing alone has, for many households, quietly climbed to consume 35-45% of take-home income on its own, before groceries, transportation, insurance, or utilities are even added. Once those get stacked on, “needs” for a real person in a real city can easily sit at 60% or higher.

This isn’t a personal failing. It’s inflation and structural cost increases doing exactly what they do — eroding the purchasing power of a fixed percentage framework built around a different economic reality. Pretending otherwise and forcing your needs into 50% by underfunding rent or skipping meals isn’t following the rule. It’s setting yourself up to fail it.

Where the Rule Genuinely Still Works

Even with the percentages shifted, the underlying structure of the rule remains one of the most useful diagnostic tools in personal finance. It forces three honest questions every month: what do I actually need to survive, what am I choosing to spend on beyond survival, and what am I setting aside for my future self. Very few people ask all three of those questions in that order without some kind of framework prompting them.

This connects directly to why most budgeting systems fail in the first place — not because the framework is wrong, but because people abandon the process the moment the numbers don’t match perfectly, instead of adjusting the ratios and keeping the habit alive.

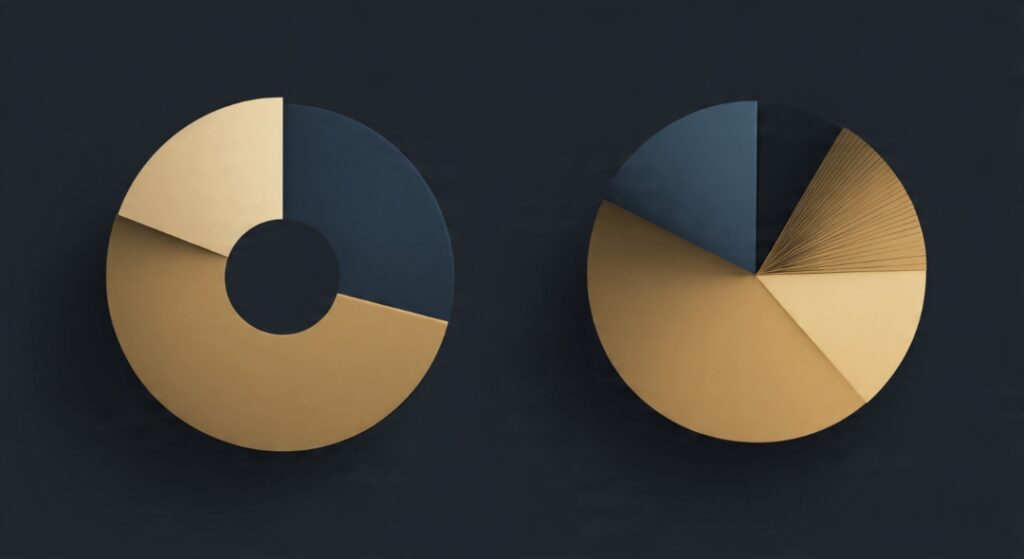

Comparison: Classic 50/30/20 vs Adjusted Real-World Version

| Category | Classic Rule | Realistic Adjusted Version |

|---|---|---|

| Needs | 50% | Often 55-65% in high-cost areas |

| Wants | 30% | Scaled down to whatever remains after needs and a protected savings floor |

| Savings/Debt | 20% | A non-negotiable minimum, even if small, rather than whatever is “left over” |

| Mindset | Fixed percentages | Fixed principle, flexible ratio based on real cost structure |

| Review Frequency | Set once and forget | Reviewed as income or major costs change |

The Wants Category Is Where Most Budgets Actually Die

People rarely blow their budget on rent. They blow it on a category that was never clearly defined in the first place. Is a work laptop a need or a want? Is a gym membership essential or optional? Is eating out twice a week a want, or has it quietly become a “need” simply because cooking every night stopped feeling sustainable?

This is closely tied to lifestyle creep — small, individually reasonable-sounding upgrades that never get categorized honestly, and quietly move from “want” to “just how I live now” without ever being reviewed as a choice. The rule doesn’t fail here. The honesty required to categorize spending correctly does.

What Nobody Tells You

Here’s the part that gets left out of most 50/30/20 explainers: the 20% savings target is often the first thing sacrificed when needs run high, and that’s exactly backwards. Savings should be treated as the least negotiable line item, not the most flexible one, because it’s the only category directly responsible for your future financial position rather than your present comfort.

Even a smaller, honest savings rate — 10% instead of 20% — protected consistently every single month, builds far more real financial security than an aspirational 20% target that gets skipped more months than it’s hit. This is the same principle behind building an emergency fund as genuine protection rather than an afterthought squeezed in only when convenient.

“A consistent 10% beats an aspirational 20% that only shows up on good months.”

Adjusting the Rule Without Abandoning It

The right response to needs eating past 50% isn’t throwing out the framework — it’s adjusting the ratio honestly and protecting the principle underneath it. This is the same discipline behind building wealth on an average salary — the real math matters more than the assumed percentages. Start by calculating your actual needs percentage instead of assuming it’s 50%. If it’s genuinely 60%, then wants and savings need to split the remaining 40% in a way that still protects at least a modest, non-zero savings rate.

This ties directly into the difference between good debt and bad debt — if needs are consuming an outsized share of income because of high-interest debt obligations rather than pure cost of living, the real fix isn’t reshuffling budget percentages, it’s addressing the debt itself as its own priority within the plan.

Why Parkinson’s Law Makes This Harder Than It Sounds

Even with a perfectly adjusted ratio, there’s a quiet force working against every budget: expenses have a tendency to rise to meet whatever income is available, regardless of the plan on paper. This is closely related to Parkinson’s Law as it applies to money — a raise or bonus often gets absorbed into slightly nicer versions of existing spending before it ever reaches the savings line, unless that savings percentage is protected automatically rather than left to willpower each month.

This sequencing echoes the logic in cash flow before assets — stabilizing the flow of money correctly comes before anything else works. Automating the savings percentage the moment income arrives — treating it like a bill rather than a leftover — is one of the few practical defenses against this tendency, regardless of what the adjusted ratio ends up being.

Now It’s Your Move

- Calculate your actual needs percentage from last month’s real spending, not an assumed 50%.

- Define what counts as a “need” versus a “want” in writing before the month starts, not while you’re deciding whether to buy something.

- Protect a savings percentage as a non-negotiable line item, even if it’s smaller than 20% to start.

- Automate that savings transfer the same day income arrives, rather than leaving it to whatever’s left at month’s end.

- Reassess your ratio whenever income or major fixed costs change — the split isn’t meant to be set once and forgotten.

- Address high-interest debt as its own priority if it’s the reason your needs percentage is inflated, rather than just shrinking your wants category around it.

- Review your categorization honestly each month, especially anything that’s quietly shifted from “want” to “just how I live now.”