- An emergency fund is the most important stop-loss you will ever set, and it is not on a trading screen — it is in a bank account.

- Freelancers, traders, and entrepreneurs need a significantly larger cushion than salaried employees, because income volatility demands more protection, not less.

- A fund that is hard to access, exposed to market risk, or mixed with daily spending money is not a real emergency fund — it just looks like one.

- The size of the fund matters less than the system that builds it consistently. Most people fail at the system, not the math.

In trading and business conversations, risk management usually means stop-losses, position sizing, and disciplined exits. The most important stop-loss most people will ever set has nothing to do with a trading screen at all — it sits in a bank account, and it is called an emergency fund.

Life does not send a warning notification before it disrupts finances. A sudden medical bill, a car breakdown, a temporary gap between jobs or clients — none of these arrive on a convenient schedule. An emergency fund exists for exactly one purpose: making sure a life crisis never escalates into a financial catastrophe layered on top of it.

This guide from the Data Pips Team breaks down a complete, practical system for building a genuine emergency fund — not just the concept of saving money, but the specific structure that determines whether that money is actually usable when an emergency hits.

What an Emergency Fund Actually Is — and Is Not

An emergency fund is a dedicated pool of cash set aside specifically for genuinely unplanned, necessary expenses. It is not a fund for upgrading a phone, booking a vacation, or jumping on a promising investment opportunity that suddenly appears. Those are separate financial goals with their own dedicated savings, not emergency money in disguise.

Think of it as a personal insurance policy that allows calm, rational decision-making during exactly the moments when panic feels like the natural response. Investopedia’s definition of an emergency fund describes it as money specifically reserved to cover the financial impact of unexpected expenses or income loss — emphasizing that its core function is protection, not growth.

This distinction matters because the moment an emergency fund starts being treated as flexible spending money or a source for “good opportunities,” it stops functioning as protection and becomes just another general savings account — one that may not actually be there when a real emergency arrives.

How Much Is Actually Enough?

A useful way to think about emergency fund size is what can be called a safety net ratio — total emergency cash divided by monthly essential expenses, including rent, food, utilities, insurance, and other genuinely non-negotiable costs.

The standard baseline recommendation is six months of essential expenses for most people with stable, predictable income. For freelancers, entrepreneurs, traders, or anyone with fluctuating or unpredictable income, twelve months is a more appropriate target. The underlying principle is straightforward: the higher the volatility in an income source, the larger the cushion needs to be to provide genuine protection.

The Consumer Financial Protection Bureau’s guidance on emergency savings reinforces this principle, noting that the appropriate size of an emergency fund depends heavily on individual circumstances, including job stability and income predictability, rather than a single fixed number that applies equally to everyone.

“Hope is not a financial strategy. An emergency fund is.”

— Data Pips Team

The Six Qualities a Real Emergency Fund Must Have

Many people technically have savings set aside, but those savings fail when an actual emergency arrives, because the fund was never structured for real emergency use. A genuine emergency fund needs to meet six specific qualities simultaneously.

Low risk. This money exists for protection, not growth. Stocks, cryptocurrency, and aggressive investment vehicles do not belong in an emergency fund, regardless of how attractive their potential returns look. The entire purpose of this money is stability, not performance.

Instantly accessible. Emergencies do not provide advance notice. Funds need to be reachable through standard banking access — transfers, ATM withdrawal, or online banking — without delay, at any time.

Quick to withdraw. There should be no significant paperwork, approval process, or waiting period standing between a genuine need and the money being available. Investopedia’s explanation of liquidity describes exactly this quality — how quickly and easily an asset can be converted to usable cash without losing value in the process.

Unaffected by market conditions. When the broader economy is under stress, that is often precisely when an emergency fund gets used most. The fund needs to hold its value reliably during exactly the kind of market downturns that might also be affecting income or job stability at the same time.

Kept independent. This money belongs in a separate account from daily spending money and any trading or investment capital. Mixing it with regular cash flow makes it far too easy to slowly spend down without a clear, deliberate decision to do so.

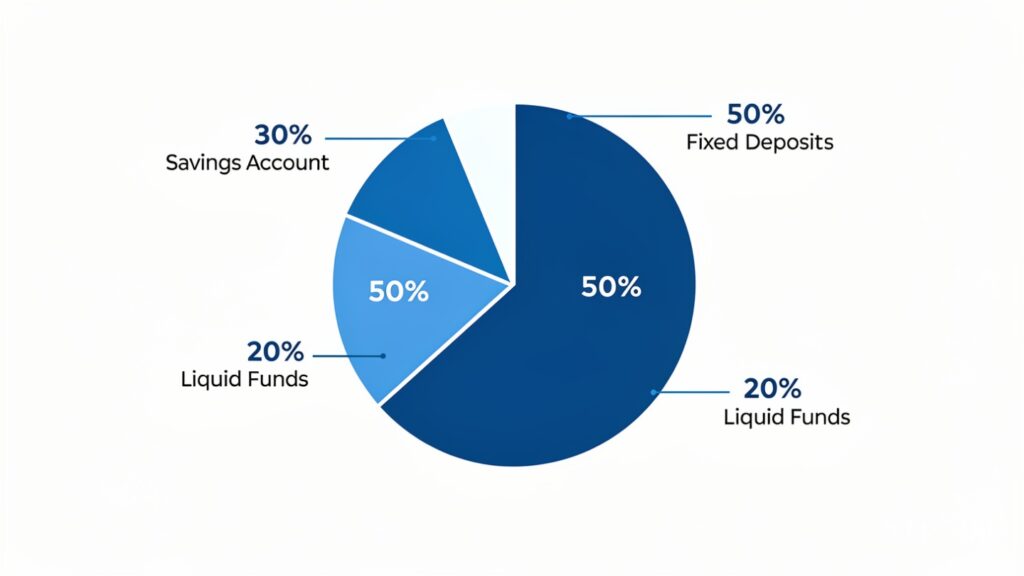

| Allocation | Where It Goes | Why |

|---|---|---|

| 30% | High-interest savings account | Instant access for immediate needs |

| 50% | Sweep-in or short-term fixed deposits | Better interest while remaining liquid |

| 20% | Liquid mutual funds or money market funds | Slightly better returns, fast withdrawal |

This kind of divided, smart allocation captures somewhat better returns than leaving everything in a single basic savings account, without sacrificing the liquidity and safety that make an emergency fund actually functional.

The Founder’s Real Lesson: Why Income Volatility Demands a Bigger Cushion

Years of relying on freelancing income alongside trading — both inherently unpredictable income sources — taught a direct lesson about emergency fund sizing that salaried-income advice often misses: a six-month cushion that works well for stable employment is frequently insufficient for genuinely volatile income.

During periods when freelance client work slowed or trading produced a difficult stretch, having a larger reserve — closer to twelve months of essential expenses — was the difference between making calm, strategic decisions and making desperate, reactive ones. Our guide on building multiple income streams covers a related strategy — diversifying income sources reduces how large a cushion is strictly necessary, since multiple income streams rarely all slow down simultaneously.

During an early period of building freelance income alongside trading, a temporary gap between client projects coincided with a difficult trading stretch in the same month. Without a dedicated emergency fund in place, that overlap would have created genuine financial pressure exactly when calm decision-making mattered most — likely pushing toward oversized, desperate trades to cover the income gap. Because a separate cushion had already been built and kept untouched for non-emergencies, the same situation instead became a manageable few weeks rather than a financial crisis layered on top of normal business volatility.

The Three-Step Method to Actually Start Building This Today

Building a fund covering six to twelve months of expenses feels overwhelming when viewed as a single, distant target. A systematic, three-step approach makes it manageable rather than paralyzing.

Track. Use a simple spreadsheet or budgeting app to identify exactly where money is currently going each month. It is genuinely difficult to fix a spending pattern that has never been clearly measured, and most people are surprised by where their money actually leaks once they track it honestly for thirty days.

Trim. Cut unnecessary recurring costs — unused subscriptions, redundant services, anything that does not provide meaningful value. For impulse purchases specifically, a simple twenty-four-hour waiting rule works well: if the desire to buy something still feels strong after a day has passed, it can be reconsidered as a genuine purchase rather than an impulsive one.

Transfer. Set up an automatic transfer into the dedicated emergency fund account, treated with the same seriousness as a mandatory bill. Starting small — even a modest fixed amount each month — and maintaining consistency matters significantly more than starting with a large, unsustainable contribution that gets abandoned after a few months.

What Nobody Tells You About Emergency Funds

1. The fund’s real value shows up in decision quality, not just available cash. The most significant benefit of a genuine emergency fund is not the money itself — it is the calm, rational decision-making it enables during a crisis. Someone with essential expenses covered for months can decline a desperate, poorly considered opportunity that someone without that cushion might feel forced to accept.

2. Most people undersize their fund because they underestimate their own expenses. Calculating monthly essential expenses accurately requires including costs that are easy to forget — annual insurance premiums divided into monthly amounts, irregular but predictable expenses, minimum debt payments. An emergency fund based on an incomplete expense calculation provides less protection than it appears to on paper.

3. A fund that earns slightly more interest but takes days to access is not actually safer. Some savings vehicles offer marginally better returns in exchange for withdrawal delays or penalties. For true emergency funds, this trade-off is rarely worth it — the entire purpose of the fund collapses if it cannot be accessed within hours during a genuine crisis.

4. Building the fund changes behavior even before it is fully funded. Many people report feeling measurably less financial anxiety once even a partial emergency fund exists — covering one or two months of expenses — well before reaching the full six to twelve month target. The psychological benefit begins accumulating long before the financial target is fully reached.

5. Income diversification and an emergency fund work together, not as substitutes for each other. Some assume that having multiple income streams reduces the need for an emergency fund entirely. In reality, the two work as complementary layers of protection — diversified income reduces the likelihood of a total income gap, while the emergency fund covers the gap if multiple income sources happen to slow simultaneously.

Emotional Freedom Is the Real Return on This Investment

An emergency fund does more than provide financial protection. It provides emotional freedom — the specific kind that allows someone to make decisions based on logic rather than desperation. For a trader, a freelancer, or any professional with income variability, knowing that basic needs are covered for an extended period changes the entire character of major decisions, removing the pressure that leads to rushed, fear-driven choices.

This connects directly to broader financial discipline. Our complete personal finance rules guide and our breakdown of the core rules of money and wealth building both build on this same foundation — protection before growth, stability before risk-taking.

This principle also extends directly into investment decision-making during uncertain periods. Our framework for investing during global uncertainty relies on exactly this kind of emergency fund as its foundation — without it, calm, disciplined investing during volatile periods becomes significantly harder to maintain.

Quick Action Steps: Start Your Emergency Fund This Week

Step 1: Calculate your true monthly essential expenses, including irregular costs divided into monthly amounts, to get an accurate target number.

Step 2: Open a separate, dedicated account for your emergency fund that is completely independent from daily spending and investment accounts.

Step 3: Set up an automatic monthly transfer into that account, starting with an amount you can sustain consistently rather than one that feels aggressive but unsustainable.

Step 4: If your income is variable — freelancing, trading, entrepreneurship — adjust your target from six months to twelve months of essential expenses.

Step 5: Once your fund reaches a meaningful size, divide it using the 30-50-20 allocation to capture modestly better returns without sacrificing liquidity.

Frequently Asked Questions

How much money should be in an emergency fund?

A general baseline is six months of essential expenses for people with stable income, and twelve months for freelancers, entrepreneurs, or anyone with variable income. The exact target depends on individual job stability, dependents, and overall financial circumstances.

Where should I keep my emergency fund?

Emergency funds should be kept in low-risk, highly liquid accounts that are easily and quickly accessible, such as high-interest savings accounts, sweep-in fixed deposits, or liquid mutual funds. Stocks, cryptocurrency, or other volatile investments are not appropriate for emergency fund money, since the principal needs to remain stable and immediately accessible.

Should my emergency fund be in the same account as my regular savings?

No. Keeping an emergency fund in a separate, dedicated account significantly reduces the temptation to spend it on non-emergency expenses and makes it easier to track progress toward your target amount without confusion from regular spending activity.

How do I start an emergency fund if I can’t save much money right now?

Start with a small, consistent automatic transfer, even if it is a modest amount each month, and build gradually. Consistency over time matters significantly more than the size of any individual contribution. Tracking and trimming unnecessary expenses first can often free up money to redirect toward this goal.

Is it okay to invest my emergency fund for better returns?

Generally, no. The purpose of an emergency fund is protection and immediate accessibility, not growth. Exposing this money to market risk through stocks or volatile investments defeats the core purpose, since the fund needs to retain its full value precisely during the kind of market downturns that might also threaten income stability.

Do freelancers and traders really need a bigger emergency fund than employees?

Yes, generally. Income volatility directly correlates with how large a protective cushion is needed. Salaried employees with predictable income can often work with a six-month target, while freelancers, entrepreneurs, and traders typically benefit from a larger twelve-month cushion due to greater income unpredictability.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial advice. Individual financial circumstances vary significantly, and emergency fund targets should be adjusted based on personal income stability, dependents, and expenses. The Data Pips Team makes no guarantees regarding financial outcomes from applying the strategies described in this article. Consult a licensed financial advisor for guidance specific to your situation.