Key Takeaways

- Wealth isn’t built by income — it’s built by the gap between what you earn and what you spend.

- Your savings rate is the single biggest lever, and it matters far more than the size of your salary.

- The real formula is simple: the gap, multiplied by time, multiplied by compounding.

- An average earner who saves 20% beats a high earner who saves nothing — every single time.

- Raising your income is the second lever, and your salary is far more negotiable than most people assume.

- It’s boring, slow, and mathematical — which is exactly why it works and most people quit.

There’s a belief that quietly keeps millions of people broke: the idea that building wealth requires a big salary. “I’ll start building wealth once I earn more,” people tell themselves, year after year, as raises come and go and their net worth stays flat. Here’s the truth the math reveals: wealth has surprisingly little to do with how much you earn, and almost everything to do with what you do with what you earn. You can build real wealth on an average salary — and the math proves it.

This isn’t a motivational promise; it’s arithmetic. In this article we’ll walk through the real math of building wealth on an ordinary income — the actual formula, the lever that matters most, and why an average earner with discipline routinely ends up wealthier than a high earner without it. No hype, no lottery tickets, just the numbers.

The Myth: Wealth Equals Income

The most expensive misconception in personal finance is that high income automatically equals wealth. It doesn’t. There are people earning large salaries who are one paycheck from disaster, and people on modest incomes quietly building serious net worth. Income is what you earn; wealth is what you keep and grow. They are not the same thing, and confusing them is why so many high earners have nothing to show for years of big paychecks.

The reason is simple: when income rises, spending usually rises to match it, a trap so common it has a name — lifestyle creep. The bigger house, the newer car, the upgraded everything absorb the raise, so the gap between earning and spending never widens. And that gap is the entire game.

“Income is what you earn. Wealth is what you keep and grow. A big salary with nothing left over builds nothing — the gap is the game, not the paycheck.”

The Real Formula for Building Wealth

Strip away all the noise and wealth-building comes down to one honest formula:

Wealth = (Income − Spending) × Time × Compounding

That’s it. The gap between income and spending is what you have to invest. Time is how long you let it grow. And compounding is the force that multiplies it. Notice what’s not the dominant term here: income by itself. Income only matters through the gap it creates. A large income with an equally large spending habit produces a tiny gap and builds almost nothing. A modest income with disciplined spending produces a healthy gap and, given time and compounding, builds real wealth. This is why the math favors the disciplined average earner over the undisciplined high earner.

Lever 1: Widen the Gap (Your Savings Rate)

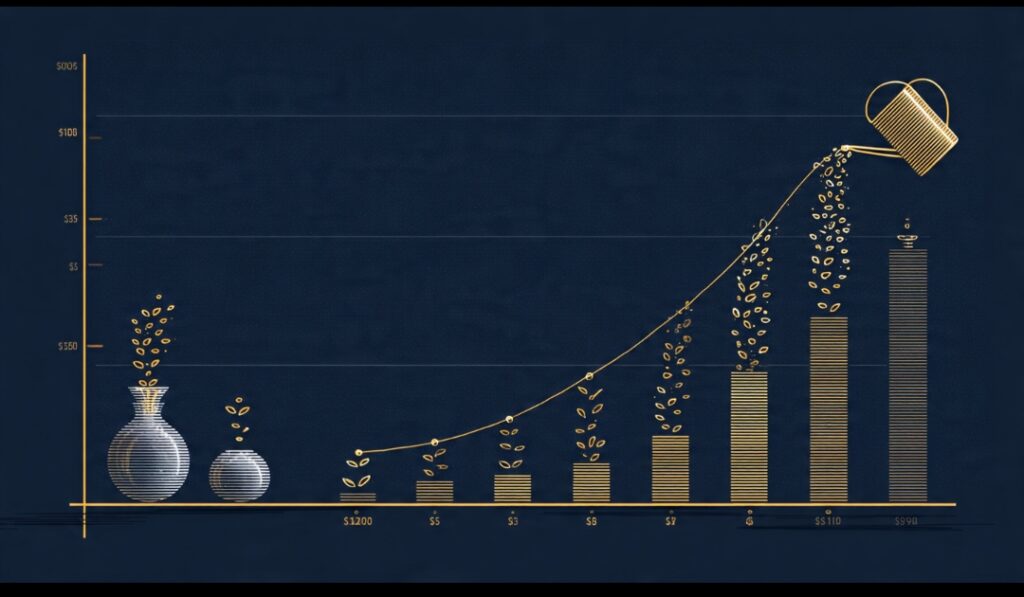

Your savings rate — the percentage of your income you keep and invest — is the single most powerful lever you control, and it matters far more than your salary size. Here’s the key insight most people miss: it’s the percentage that matters, not the dollar amount. Someone saving 20% of an average salary is building wealth at a meaningful rate. Someone saving 2% of a large salary barely is. The rate is what determines your trajectory.

Consider the math in illustrative terms. Imagine consistently investing a portion of an average income each month and earning a steady long-term rate of return of around 7%. Over 30 years, thanks to compounding, that steady stream can grow into a sum many times larger than the total you contributed — often several hundred thousand in the same currency you’re saving in, from contributions that never required a big salary. The exact figure is just illustration, not a promise, but the principle is ironclad: a consistent savings rate on an ordinary income, given enough time, produces substantial wealth. Protecting that rate is exactly why an automated system beats willpower, the logic behind a budgeting system that actually works.

And this reframes the whole goal. You don’t need to chase a higher income to start building wealth — you need to widen your gap today, at your current salary, by keeping lifestyle inflation in check and consciously deciding to keep a meaningful slice of what you earn.

“Your savings rate, not your salary, sets your trajectory. Saving 20% of an average income beats saving 2% of a large one — the percentage is the whole story.”

Lever 2: Give It Time to Compound

The second lever is time, because compound interest does the real heavy lifting. When your money earns returns, and those returns earn returns, growth accelerates — slowly at first, then dramatically. The catch is that most of the magic happens late, which is why the early years feel discouragingly slow and so many people quit before the acceleration kicks in. That frustrating early stretch is the exact trap we mapped in why compounding feels slow at first.

The practical takeaway from the time value of money is simple: start now, and don’t stop. Time is the one input you can never get back, and it’s freely available to the average earner just as much as the wealthy one. Someone on a modest salary who starts early and stays consistent will often out-compound a high earner who starts late — because time, not income, is doing most of the work. This is also how ordinary consistency turns into real assets, the transition covered in going from active income to passive wealth.

Lever 3: Raise Your Income (The Underused Lever)

Widening the gap has two sides: spend less, or earn more. And while savings rate is the foundation, growing your income accelerates everything — a bigger income with a maintained savings rate means a bigger gap feeding the machine. The mistake is treating your income as fixed. It usually isn’t.

Here’s a truth most salaried people never fully act on: your salary is far more negotiable than you assume, and proactively raising it is one of the most underused wealth levers there is. Most people passively accept whatever raise they’re given, never realizing that the value they deliver — not the number on their current contract — is what they can actually command. The people who build wealth faster on a salary are often the ones who deliberately increase their earning power: by becoming demonstrably more valuable, by making that value visible, and then by calmly and confidently asking to be paid what that value is worth. Asking for a raise, backed by real contribution, is not greedy or awkward — it’s a legitimate, powerful financial move that most people leave on the table for years. Combine that with building skills that compound your value, the idea behind turning skill into a wealth machine, and you widen the gap from both ends at once.

| High income, low savings rate | Average income, high savings rate |

|---|---|

| Big paycheck, tiny gap | Modest paycheck, healthy gap |

| Spending rises with every raise | Spending held steady, gap grows |

| Little invested, little compounding | Consistent investing, full compounding |

| Looks rich, isn’t | Looks ordinary, quietly wealthy |

| Ends with little | Ends genuinely wealthy |

What Nobody Tells You

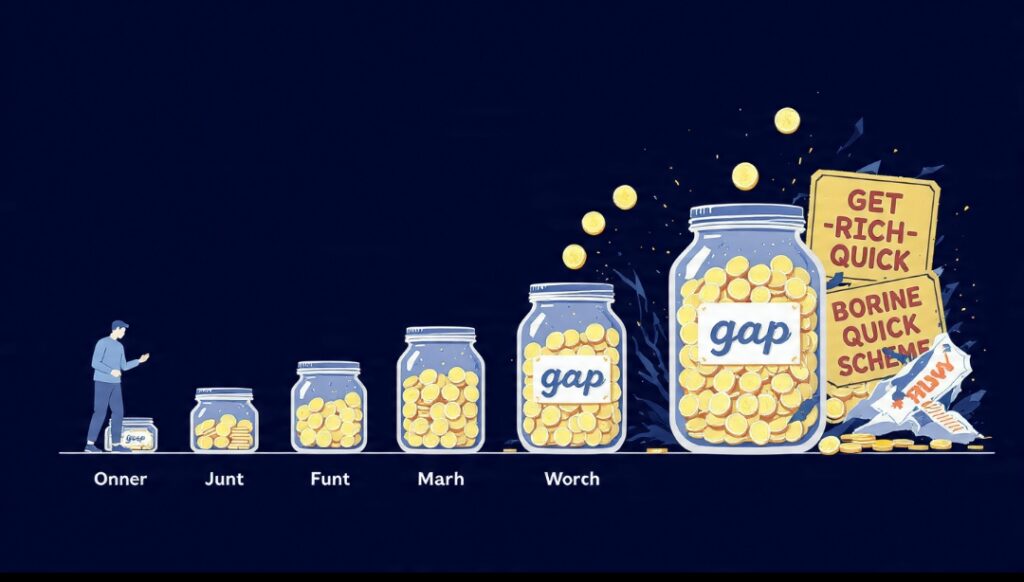

Here’s the honest, slightly disappointing truth: building wealth on an average salary is boring. There’s no dramatic moment, no lucky windfall, no secret. It’s the same unglamorous actions repeated for years — keep the gap wide, invest consistently, let time compound, and don’t touch it. That boredom is precisely why most people never do it. They want excitement and speed, so they chase lottery-ticket schemes and get-rich-quick promises, while the quiet, mathematical path sits ignored, working perfectly for anyone patient enough to walk it.

And this is the real reason wealth on an average salary comes down to psychology, not income. The math is trivially simple — a child could understand the formula. The hard part is the discipline to keep the gap open when everyone around you is inflating their lifestyle, and the patience to let compounding work through the slow years. Beating the urge to spend today for a wealthier tomorrow is the same battle as overcoming present bias, and winning it consistently is what small, repeated financial habits are built for, exactly like the 1% rule of daily progress. The person who wins isn’t the one with the biggest salary — it’s the one who solved the math problem with boring, relentless consistency.

Now It’s Your Move

You do not need a bigger salary to start building wealth. You need to put the math on your side — widen the gap between what you earn and what you spend, invest that gap consistently, give it time to compound, and grow your income where you can. That’s the entire formula, and it works on an average income for anyone with the discipline to run it.

- Calculate your gap. Know exactly how much of your income you currently keep. That number is your starting point.

- Raise your savings rate. Widen the gap by even a few percent this month, and guard it against lifestyle creep.

- Automate the investing. Put the gap to work automatically so it compounds without relying on willpower.

- Give it real time. Start now, stay consistent, and don’t interrupt the compounding.

- Grow your income deliberately. Build valuable skills and negotiate your worth to widen the gap from both ends.

The person quietly building real wealth on an ordinary paycheck isn’t smarter or luckier than everyone else — they just understood the math and had the patience to let it work. The formula is available to you right now, at the salary you already earn. Start widening your gap today, and let the boring, unstoppable math do the rest.

Yes, because wealth is built by the gap between what you earn and what you spend, multiplied by time and compounding, not by income alone. An average earner who consistently saves a meaningful percentage and invests it over many years can build substantial wealth, often ending up wealthier than a high earner who saves little. The salary size matters far less than your savings rate, your consistency, and the time you give compounding to work.

The core formula is the gap between your income and spending, multiplied by time, multiplied by compounding. The gap is what you have available to invest, time is how long you let it grow, and compounding is the force that multiplies it. Income only matters through the gap it creates, so a modest income with disciplined spending can build more wealth than a large income with heavy spending. It is a math problem solved by consistency.

Because your savings rate is the percentage of income you actually keep and invest, and it determines your trajectory regardless of salary size. Someone saving 20% of an average income builds wealth meaningfully, while someone saving 2% of a large income barely does. Since spending tends to rise with income through lifestyle creep, a high salary often produces only a tiny gap. The rate you keep, not the amount you earn, is what compounds into wealth.

Compounding means your returns earn their own returns, so growth accelerates over time, slowly at first and then dramatically. This heavy lifting is available to anyone regardless of income, so a modest earner who starts early and invests consistently can out-compound a high earner who starts late. Time is the key input, and it is freely available to everyone. The main challenge is patience, since most of the growth happens in the later years after a slow start.

Both, since widening the gap has two sides, but start with your savings rate because it is the lever you control immediately at your current income. Spending less raises your gap today, while earning more accelerates everything if you maintain your savings rate rather than inflating your lifestyle. Growing your income through more valuable skills and negotiating your salary is a powerful and underused lever, so ideally you widen the gap from both ends over time.

Far more than most people assume. Many salaried workers passively accept whatever raise they are offered, not realizing that the value they deliver is what they can actually command, not just their current contract. Becoming demonstrably more valuable, making that value visible, and then confidently asking to be paid accordingly is a legitimate and powerful financial move. Proactively raising your income, backed by real contribution, is one of the most underused wealth levers available to salaried people.

Because they confuse income with wealth and let spending rise to match every raise, a trap called lifestyle creep, so their gap never widens. The math of wealth-building is simple, but it is boring and slow, requiring years of consistent saving and patience through the early period when compounding feels ineffective. Most people want speed and excitement, so they neglect the quiet, disciplined path. The failure is almost always about psychology and consistency, not income.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial or investment advice. The numerical examples are simplified illustrations, not predictions or guarantees of any specific return, and all investing involves risk, including the loss of capital. Returns vary and are never guaranteed. Individual circumstances differ, so always do your own research and consider consulting a qualified financial professional before making money decisions.