Key Takeaways

- Most people think about money as something to earn and spend. Businessmen think about money as a tool to build more money.

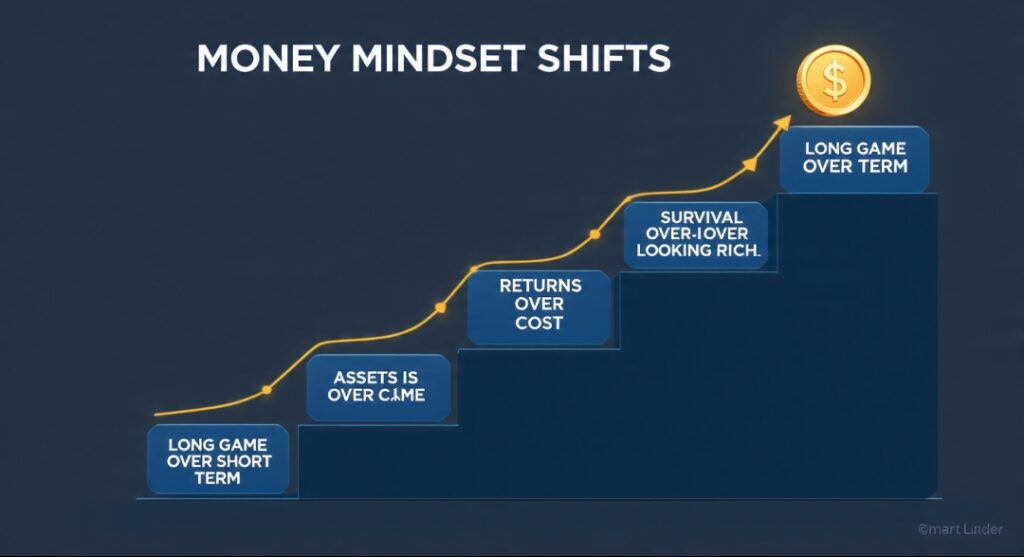

- The biggest mental shift is from focusing on income to focusing on assets — things that put money in your pocket over time.

- Businessmen prioritize cash flow and survival over looking rich, understanding that staying in the game matters more than appearing successful.

- They think in terms of return and multiplication, asking not “what does this cost?” but “what will this produce?”

- These are learnable mindset shifts, not inborn traits — anyone can start thinking about money the way builders do.

Two people can earn the exact same salary, and ten years later one is wealthy while the other is broke. The difference is rarely how much they made. It is how they thought about what they made. The way a businessman’s mind processes money is fundamentally different from how most people are taught to think about it, and that difference compounds over a lifetime into completely different outcomes.

Here is the uncomfortable truth: most of us were never taught to think about money correctly. We learned to earn it, spend it, and maybe save a little. But the people who build real wealth operate on a different mental operating system entirely. They look at the same dollar you do and see something completely different. And the good news is that this way of thinking is learnable. It is not about being born rich or being a genius. It is about a handful of mindset shifts.

The Data Pips Team is going to break down exactly how businessmen think about money differently — the specific mental shifts that separate the people who build wealth from the people who merely earn and spend. This is not theory. These are the practical thinking patterns behind real financial building. Let us get into it.

Shift 1: Money Is a Tool, Not a Goal

Most people treat money as the destination. You earn it, and the purpose of earning it is to have it and spend it. Money is the prize at the end.

Businessmen flip this. To them, money is not the prize — it is a tool. It is raw material, like wood to a carpenter or seeds to a farmer. The point of having money is not to hold it or spend it on stuff; the point is to use it to build something that produces more money. A dollar in a businessman’s hand is not for buying — it is for deploying.

This single shift changes everything downstream. When money is a goal, every dollar that arrives is asking “what can I buy?” When money is a tool, every dollar that arrives is asking “what can I build with this?” The first question leads to a nicer phone and an emptier account. The second question leads to assets, businesses, and growing wealth.

This does not mean businessmen never enjoy their money — they do. But they draw a hard line between money that is meant to be deployed and money that is meant to be enjoyed, and in the building years, the vast majority goes toward deployment. They delay the enjoyment because they understand that money used as a tool today becomes far more money to enjoy tomorrow. The ordinary mind spends first and saves what is left. The builder’s mind deploys first and spends what is left.

— Data Pips Team

Shift 2: Focus on Assets, Not Just Income

This is perhaps the most important shift of all, and most people miss it entirely. The average person is obsessed with income — the salary, the raise, the monthly paycheck. Income feels like the whole game. Earn more, and you win.

Businessmen know income is only half the picture, and arguably the smaller half. They are obsessed with assets. An asset is something that puts money in your pocket — a business, a rental property, an investment, intellectual property, a skill that generates ongoing income. The businessman’s central question is not just “how do I earn more?” but “how do I acquire more assets that earn for me?”

Here is why this matters so much. Income from a job stops the moment you stop working. It is you trading time for money, and your time is limited. But assets keep producing whether you work or not. They earn while you sleep. So while the average person tries to climb the income ladder one rung at a time, the businessman is busy buying and building machines that generate income on their own. One is running on a treadmill; the other is building treadmills that run by themselves.

The flip side of assets is liabilities — things that take money out of your pocket. The fancy car, the oversized house, the expensive lifestyle. The ordinary mind, when income rises, immediately buys more liabilities. The builder’s mind, when income rises, buys more assets, and lets those assets eventually pay for the liabilities. This distinction — assets feed you, liabilities drain you — is the financial backbone of how businessmen think. Building income that does not depend on your daily labor is the heart of it, something we explore in our guide on passive income assets and monthly cash flow.

Shift 3: Cash Flow and Survival Beat Looking Rich

Walk through any city and you will see people who look wealthy — expensive cars, designer clothes, the appearance of success. Many of them are one bad month away from disaster. They optimized for looking rich. Businessmen optimize for something completely different: staying in the game.

A businessman understands that the first rule of winning is not getting knocked out. And what knocks businesses and individuals out is not lack of profit on paper — it is running out of cash flow. Cash flow is the actual money moving in and out, the oxygen of any financial life. You can look rich, even be rich on paper, and still suffocate if the cash stops flowing.

This is why experienced businessmen are almost obsessive about cash flow and survival. They keep reserves. They avoid overextending. They would rather look modest and have a deep financial cushion than look impressive and live on the edge. They know that a business can be profitable and still die if cash gets too tight, because survival depends on liquidity, not appearances. Maintaining a steady frequency of money coming in — from any source — matters more than any single big win.

The ordinary mind asks “how can I look successful?” The builder’s mind asks “how do I make sure I never get knocked out?” This is not fear — it is respect for the game. The businessman knows that as long as he survives, he can keep playing, keep building, keep compounding. Get knocked out, and all of it ends. Looking rich is a vanity; staying solvent is a strategy. This deep respect for protecting your capital is a mindset we explore further in our guide on the psychology of money and respecting capital.

Shift 4: Think in Returns, Not Costs

When most people consider spending money, they ask one question: “What does this cost?” The price is the whole consideration. Cheaper is better, expensive is worse, and the goal is to spend as little as possible.

Businessmen ask a completely different question: “What will this produce?” They think in terms of return on investment — not what something costs, but what it gives back. A businessman will happily spend a large amount on something that returns even more, and refuse to spend a tiny amount on something that returns nothing. The price tag alone tells them almost nothing; the return is what matters.

This reframes every financial decision. A course that costs money is not an “expense” if it teaches a skill that earns many times its price — it is an investment. A tool that costs money is not a cost if it saves or generates more than it costs. Meanwhile, a cheap purchase that produces nothing is not a “good deal” just because it was inexpensive; it is pure consumption. The businessman evaluates money flowing out by what flows back, not by the size of the outflow alone.

This is why businessmen can seem simultaneously generous and stingy. They will invest heavily in things that produce returns — talent, tools, opportunities, skills — and be ruthlessly tight on things that simply drain money with no return. It looks inconsistent until you understand the underlying logic: every dollar is judged by what it brings back. Cost is only half the equation, and the half most people fixate on is the less important one. This same value-first logic applies to building skills, which we cover in our guide on compounding skill into a wealth machine.

The Same $1,000, Two Different Minds

Picture two people who each unexpectedly receive $1,000. Watch how differently their minds process the exact same money.

The ordinary mind sees $1,000 as buying power. The questions are about consumption: a new gadget, some clothes, a nice weekend, maybe a little saved if there is willpower left over. Within a few weeks, the $1,000 is gone, converted into things that produce nothing. The money was treated as a goal — something to have and spend.

The builder’s mind sees $1,000 as raw material. The questions are about production: Can this buy a skill that earns more? Can it start or grow something? Can it be placed where it multiplies? The $1,000 is not spent on consumption — it is deployed as a tool, aimed at producing more than $1,000 over time. The money was treated as a seed, not a prize.

Now run this forward across a lifetime, across thousands of such decisions. The ordinary mind converts money into stuff, again and again, and stays roughly where it started. The builder’s mind converts money into assets and returns, again and again, and compounds steadily upward. Same money entering both lives — completely different thinking, completely different destinations.

The lesson: Wealth is built less by how much money flows into your life and more by how your mind processes that money when it arrives. Change the processing, and you change the destination.

Shift 5: Patience and the Long Game

Perhaps the deepest difference is the time horizon. Most people think about money in the short term — this month, this purchase, this paycheck. The mental frame rarely extends far beyond the immediate.

Businessmen think in years and decades. They are playing a long game, and they understand the most powerful force in finance: compounding. They know that money used wisely grows on itself, and that small advantages, repeated and reinvested over long periods, become enormous. So they are willing to delay gratification today for far greater results tomorrow, because they can actually see the long arc that most people ignore.

This patience is not passive waiting — it is active, strategic delay. The businessman reinvests profits instead of spending them, knowing reinvestment compounds. He builds slowly and deliberately, knowing that what grows steadily over years beats what spikes and crashes. He measures success not by where he is this month, but by where he is heading over the next five and ten years. The short-term sacrifices feel small to him because the long-term vision is so clear. This is the exact principle behind our guide on the 1% rule and daily compounding — tiny gains, relentlessly repeated, becoming remarkable over time.

The ordinary mind asks “what can I have now?” The builder’s mind asks “what will this become if I let it grow?” This difference in time horizon, more than almost anything else, explains why patient builders end up wealthy while impatient earners stay stuck. The money behaves according to the time frame you give it — rush it, and it scatters; give it years, and it compounds.

— Data Pips Team

What Nobody Tells You About the Money Mindset

1. It’s Learnable, Not Inborn

The biggest myth is that some people are just “good with money” by nature. The truth is that these are learned thinking patterns, not genetic gifts. Every shift described here can be practiced and adopted by anyone willing to retrain how they think. People who grew up around this thinking absorbed it early, which gives them a head start, but the thinking itself is fully learnable at any age. You are not locked out by your background — you are one mindset shift away from starting.

2. It Feels Uncomfortable at First

Thinking like a builder often means doing the opposite of what feels natural — deploying money instead of spending it, delaying enjoyment, looking modest while building quietly. This feels uncomfortable, even unnatural, especially when those around you are spending freely and looking successful. That discomfort is normal and temporary. It is the feeling of rewiring a habit, and it fades as the new thinking becomes second nature and the results start to show.

3. Small Money Thinking and Big Money Thinking Are the Same

People assume this mindset only applies once you have a lot of money. Wrong. The thinking patterns work identically whether you are processing $100 or $100,000 — the scale changes, the principles do not. In fact, the people who build wealth started applying this thinking when they had very little. Waiting until you are rich to think like a builder is backwards; thinking like a builder is how you get there in the first place.

4. It’s Not About Being Cheap

This mindset is often confused with stinginess, but they are completely different. Being cheap is refusing to spend out of fear. Thinking like a builder is spending strategically on what produces returns while avoiding what merely drains. A builder will spend large amounts willingly when the return justifies it, something a merely cheap person never would. The goal is not to hoard money but to deploy it intelligently, which sometimes means spending boldly and sometimes means spending nothing.

5. The Mindset Matters More Than the Income

The hardest truth to accept: how you think about money matters more than how much you make. High earners with poor money thinking stay broke, while modest earners with builder thinking quietly accumulate wealth. This is liberating, because it means you do not have to wait for a big income to start building — you can start with the thinking, right now, at whatever income you have. The mindset is the lever; income is just one input it acts upon.

How to Start Thinking Like a Builder

Quick Action Steps

- Treat money as a tool. When money arrives, ask “what can I build with this?” before “what can I buy?” Train the deploy-first instinct.

- Hunt for assets. Shift your focus from just earning income to acquiring things that produce income — skills, investments, businesses, anything that pays you over time.

- Protect your survival. Prioritize cash flow and reserves over looking successful. Staying in the game beats appearing to win it.

- Judge by return, not cost. When spending, ask “what will this produce?” not just “what does this cost?” Invest in what returns; refuse what merely drains.

- Stretch your time horizon. Think in years and decades, not weeks. Let compounding work by reinvesting and delaying gratification for far greater future results.

- Start now, at any income. Don’t wait to be rich to think like a builder. Apply this thinking to whatever money you have today — that’s how building begins.

- Build the daily habits. Wealth thinking is reinforced by consistent daily patterns, the kind explored in our guide on the daily thinking patterns of successful businessmen.

Frequently Asked Questions

The core difference is that most people think about money as something to earn and spend, while businessmen think about money as a tool to build more money. This leads to several specific shifts: they focus on acquiring assets (things that produce income) rather than just chasing income; they prioritize cash flow and survival over looking rich; they judge spending by what it will produce (return) rather than just what it costs; and they think in years and decades, harnessing compounding, rather than in the short term. The remarkable thing is that two people earning the same amount can end up with completely different wealth purely because of how their minds process the money they receive.

Arguably the most important shift is moving from focusing on income to focusing on assets. Most people are obsessed with their salary and earning more, but income from a job stops the moment you stop working — it is trading limited time for money. Assets, by contrast, are things that put money in your pocket whether you work or not: businesses, investments, rental properties, income-generating skills. They earn even while you sleep. While the average person climbs the income ladder one rung at a time, the businessman builds and acquires assets that generate income on their own. Shifting your central question from “how do I earn more?” to “how do I acquire assets that earn for me?” changes your entire financial trajectory.

Businessmen care obsessively about cash flow because it is what keeps you in the game — and the first rule of winning is not getting knocked out. Cash flow is the actual money moving in and out, the oxygen of any financial life. What kills businesses and individuals is rarely lack of profit on paper; it is running out of cash. You can look rich, even be rich on paper, and still collapse if the cash stops flowing. This is why experienced businessmen keep reserves, avoid overextending, and would rather look modest with a deep cushion than look impressive while living on the edge. They understand that survival depends on liquidity, not appearances, and that as long as they survive, they can keep building and compounding.

Yes, absolutely. The biggest myth is that some people are just naturally “good with money,” but these are learned thinking patterns, not genetic gifts. Every mindset shift — treating money as a tool, focusing on assets, prioritizing survival, judging by return, thinking long-term — can be practiced and adopted by anyone willing to retrain how they think. People who grew up around this thinking absorbed it early and have a head start, but the thinking itself is fully learnable at any age and any income level. In fact, the thinking works the same whether you are processing a small amount or a large one, so you can start applying it right now with whatever money you have. You are not locked out by your background.

No, they are completely different. Being cheap is refusing to spend out of fear, avoiding all spending regardless of value. Thinking like a builder is spending strategically — investing willingly and even boldly in things that produce returns, while ruthlessly avoiding things that merely drain money with no return. A builder will happily spend a large amount on a skill, tool, or opportunity that returns many times its cost, something a merely cheap person would never do. At the same time, they refuse to waste money on pure consumption that produces nothing. The goal is not to hoard money but to deploy it intelligently, judging every dollar by what it brings back rather than simply minimizing all spending.

Patience is crucial because of compounding — the most powerful force in finance. Money used wisely grows on itself, and small advantages, repeated and reinvested over long periods, become enormous. Businessmen think in years and decades rather than weeks, which lets them harness this. They reinvest profits instead of spending them, build slowly and deliberately, and measure success by where they are heading over the next five to ten years rather than this month. The short-term sacrifices feel small because the long-term vision is so clear. This difference in time horizon largely explains why patient builders end up wealthy while impatient earners stay stuck — money behaves according to the time frame you give it. Rush it and it scatters; give it years and it compounds.

No — and this is one of the most liberating truths about money. How you think about money matters more than how much you make. High earners with poor money thinking often stay broke, while modest earners with builder thinking quietly accumulate wealth over time. The thinking patterns work identically whether you are processing a small amount or a large one; only the scale changes, not the principles. In fact, the people who build wealth typically started applying this thinking when they had very little. Waiting until you are rich to think like a builder is backwards — thinking like a builder is how you get there in the first place. You can start with the mindset right now, at whatever income you have, and let it guide every financial decision going forward.

Now It’s Your Move

Two people, the same salary, completely different outcomes a decade later. Now you understand why. It was never mainly about how much they earned — it was about how their minds processed money. The businessman runs on a different mental operating system, and you have just seen exactly what it looks like: money as a tool not a goal, assets over income, survival over appearances, returns over costs, and the long game over instant gratification.

None of this requires being born rich, being a genius, or already having wealth. These are learnable shifts in thinking — ways of looking at the same dollar you already handle and seeing something different. The person who sees money as a seed to plant rather than a prize to spend will, over a lifetime of thousands of small decisions, end up somewhere completely different from the person who never made that shift. And the beautiful part is that the shift is available to you right now, at whatever income you have.

The mistake most people make is waiting — waiting for a higher salary, a windfall, the “right time” to start thinking about money seriously. But the thinking is the cause, not the result. You do not get the builder’s mindset after you become wealthy; you become wealthy partly because you adopted the builder’s mindset early. The income is just one input. The thinking is the lever that moves everything.

So start where you are. The next time money arrives in your life, however small, pause and ask the builder’s questions: What can I build with this? Is this an asset or a liability? Does this protect my survival? What will this produce? What will it become if I let it grow? Those questions, asked consistently over years, are quite literally how wealth gets built — one reframed decision at a time.

You now understand how businessmen think about money differently. The only thing left is to start thinking that way yourself — today, with whatever you have.

For your next steps, deepen this with our guides on the daily thinking patterns of successful businessmen, the power of the 1% rule and compounding, and how to build multiple income streams that turn this mindset into real assets.