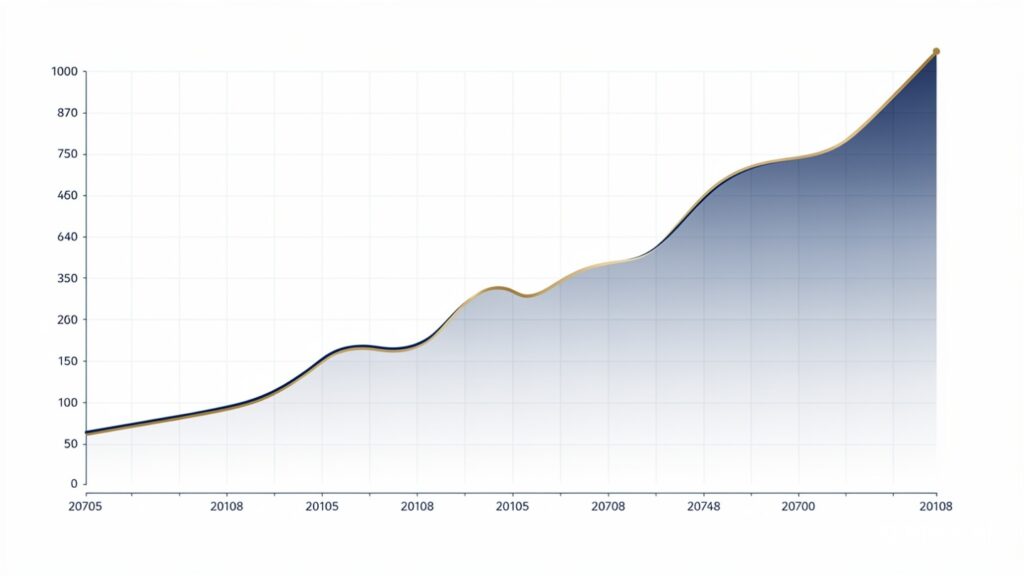

- Compounding is back-heavy — the most dramatic growth happens in the final years of the investment period, which is exactly why most people quit too early.

- Starting early matters more than starting big. Time, not contribution size, is the most valuable input in the compounding equation.

- The real goal of understanding compounding is shifting from actively trading time for money to owning assets that generate income independently.

- High-interest debt is compounding working in reverse — against you, not for you.

In a world saturated with get-rich-quick promises, genuine financial independence remains a marathon, built almost entirely on a single mathematical phenomenon: compounding. Understanding how compounding actually works is the first real step toward exiting the cycle of trading hours for money and building something that continues generating wealth independently of daily effort.

This is not a motivational concept. It is straightforward mathematics, available to anyone with a plan and the patience to follow it consistently — not a secret reserved for financial insiders or those who started with significant capital.

This guide from the Data Pips Team breaks down exactly how compounding works, why most people abandon it right before it would have paid off, and the practical shift from active income to genuinely passive wealth.

What Compounding Actually Is

Compounding is the process where the earnings on an investment get reinvested to generate their own additional earnings. Instead of earning a return only on the original principal amount, an investor begins earning returns on previously earned returns as well — commonly described as earning “interest on interest.”

Investopedia’s definition of compounding confirms this mechanism is the engine behind nearly all meaningful long-term wealth accumulation, distinguishing it clearly from simple interest, where returns only ever apply to the original amount invested.

Over a short period, the visible progress from compounding looks almost negligible — barely distinguishable from random market noise. Over decades, however, this same mechanism transforms modest, consistent contributions into substantial accumulated wealth, precisely because each year’s growth builds directly on top of all previous growth rather than starting fresh.

The Three Pillars of Compounding Success

1. The Advantage of Starting Early

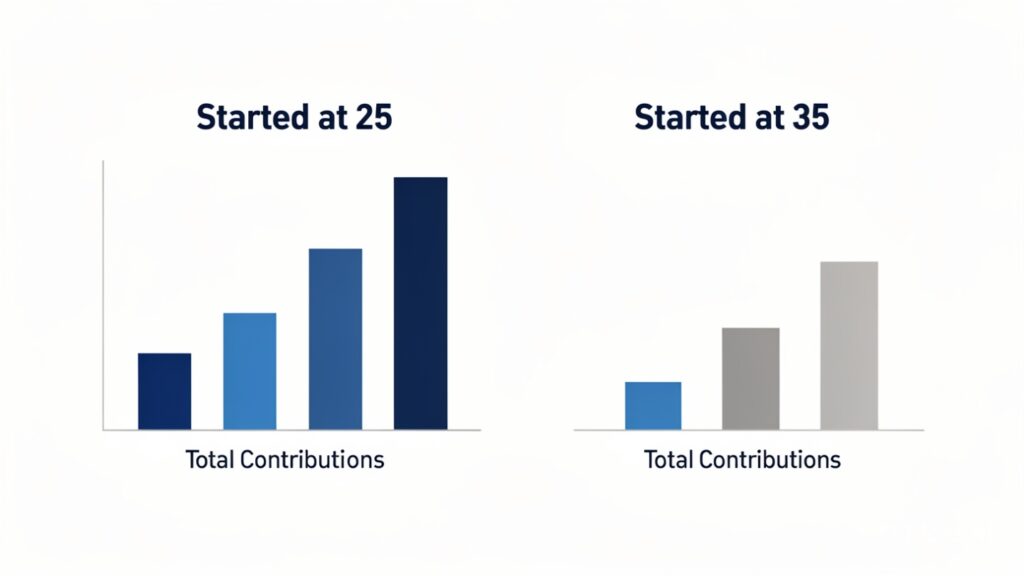

In long-term wealth building, time is a more valuable input than the actual size of any individual contribution. The earlier consistent investing begins, the less total money needs to be contributed to reach a given financial goal, because compounding has more time to work on each dollar invested.

An individual who begins investing in their mid-twenties will typically accumulate significantly more wealth by their sixties than someone who starts a decade later, even if the later starter contributes considerably more money overall. Compounding requires a long runway to produce its most dramatic results — which is exactly why delaying the start, even by a few years, carries a real and often underestimated cost.

2. Consistency Over Intensity

Building substantial wealth does not require a single large windfall. It requires the discipline to consistently save and invest a fixed portion of income, regardless of short-term market conditions. Staying committed to a long-term investment plan through both upward and downward market cycles ensures that an investor captures the broader, long-term growth trend of the economy rather than trying to time entries and exits around short-term volatility.

3. The Psychology of Patience

The biggest threat to compounding is not a difficult market — it is human emotion. Most investors abandon their investment plan during the first several years specifically because the visible results do not yet feel dramatic enough to justify the discipline required. Compounding is mathematically back-heavy, meaning the most significant, visible growth concentrates in the final stretch of the investment timeline. Genuine success requires the emotional steadiness to stay committed during the quiet, unglamorous early years while others abandon their own plans.

“Compounding is not a secret reserved for the wealthy. It is a universal law available to anyone with a plan and the patience to follow it.”

— Data Pips Team

Why Most People Quit Right Before Compounding Pays Off

This is the single most expensive mistake in long-term wealth building, and it happens predictably. Because compounding’s growth curve is exponential rather than linear, the early years produce results that genuinely look unimpressive compared to the effort invested. A consistent investor might check their progress after two or three years and see growth that feels barely worth the discipline required to maintain it.

That feeling is mathematically expected, not a sign that the process is failing. The dramatic, visible acceleration that defines compounding’s reputation happens disproportionately in the later years of a long investment timeline — which means abandoning the process during the early, unimpressive-looking phase guarantees missing the exact results the entire strategy was built to produce.

| Investor Type | Behavior | Outcome |

|---|---|---|

| Starts early, stays consistent | Maintains contributions through market cycles | Captures the full compounding curve |

| Starts late, contributes more | Higher monthly contributions, shorter timeline | Often ends with less total wealth despite more input |

| Starts early, quits early | Abandons plan during the unimpressive early years | Misses the back-loaded growth entirely |

The Founder’s Real Lesson: Discipline Beats Timing

Years of building income through freelancing and trading reinforced a direct, sometimes uncomfortable lesson about compounding: the temptation to interrupt a consistent savings or investment plan during a slow month, a tempting purchase, or a moment of doubt about the strategy is constant — and giving in to that temptation even occasionally creates damage far larger than it appears to in the moment.

The investors and savers who built genuine long-term wealth were rarely the ones who picked the perfect entry point or the single best-performing asset. They were consistently the ones who kept contributing through uncertain periods, resisted the urge to withdraw during temporary downturns, and trusted that the mathematics would eventually produce visible results — even when years of evidence had not yet arrived to confirm that trust.

Early in building consistent savings habits, a tempting short-term opportunity prompted withdrawing accumulated savings that had been compounding for several years, with the intention of “starting fresh” afterward with even more discipline. The opportunity itself produced modest results. The larger, harder-to-see cost was the years of accumulated compounding that had been reset to zero — a setback that took considerably longer to recover from than the withdrawal itself had taken to spend. That single decision became the clearest possible lesson in why interruption, not poor returns, is usually the actual enemy of long-term compounding.

Shifting From Active Income to Passive Assets

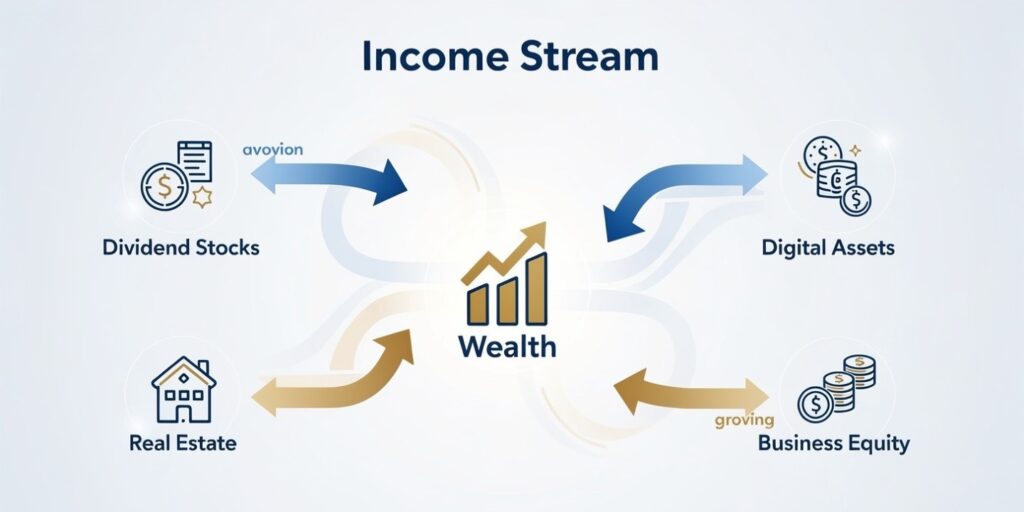

The ultimate purpose of understanding compounding is making the transition from actively trading time for money to owning assets that generate income independently of daily effort. Several specific approaches support this shift directly.

Dividend reinvestment. Automatically reinvesting dividend payments to purchase additional shares accelerates compounding by increasing the asset base generating future returns, rather than treating dividends as spendable cash.

Real estate income reinvestment. Using rental income to acquire additional property, rather than spending it as it arrives, applies the identical compounding principle to physical assets.

Digital and content assets. Building content, systems, or digital products that continue generating value without requiring proportional ongoing time investment represents a more modern application of the same underlying principle — work invested once continuing to pay returns indefinitely.

Business equity. Owning a stake in a growing enterprise, whether through direct ownership or equity investment, allows capital to compound through business growth rather than relying solely on traditional savings vehicles.

Our complete guide on passive income assets breaks down ten specific options across this entire risk and complexity spectrum in significantly more practical detail.

What Nobody Tells You About Building Compound Wealth

1. High-interest debt is compounding working against you. The exact mechanism that builds wealth when applied to investments actively destroys it when applied to debt, particularly high-interest credit obligations. Carrying significant high-interest debt while simultaneously trying to build investment compounding means fighting the same mathematical force in two opposite directions at once — eliminating that debt should generally precede aggressive investing.

2. “Passive” income still requires real upfront effort. Investopedia’s definition of passive income clarifies that even classic passive income sources typically demand significant initial capital, research, or active setup before becoming genuinely low-maintenance. Expecting effortless results from the very beginning leads to disappointment and premature abandonment of strategies that simply needed more time to mature.

3. Automating contributions removes the single biggest point of failure. The decision to invest consistently, made fresh every single month, is vulnerable to mood, temptation, and rationalization. Setting up automatic transfers into an investment account removes that recurring decision entirely, protecting the compounding process from the exact human inconsistency that derails most long-term plans.

4. Thinking in decades changes which information actually matters. Daily financial news and short-term market movements become largely irrelevant to an investor genuinely focused on a ten or twenty-year horizon. Constant exposure to short-term noise tends to trigger exactly the kind of premature, emotional decisions that interrupt compounding before it has time to work.

5. The hardest discipline is not contributing — it is not withdrawing. Many investors successfully maintain consistent contributions but undermine their own progress by withdrawing accumulated gains during the active accumulation phase for non-essential purchases. Our breakdown of the specific mistakes that sabotage compounding covers this exact pattern and several others in considerably more depth.

Practical Steps to Start Compounding Today

Eliminate high-interest debt first, since compounding works directly against an investor while that debt remains outstanding. Automate savings and investment contributions so the decision to invest does not need to be remade emotionally every single month. Think in decades rather than days, deliberately limiting exposure to short-term financial noise that tends to trigger premature, reactive decisions. During the active accumulation phase, avoid withdrawing gains, allowing the full compounding mechanism to continue working uninterrupted.

None of these steps require significant starting capital. Our guide on the 1% rule and daily compounding habits covers how this same exponential mechanism applies just as powerfully to skill development and consistent habits as it does to financial capital, meaning the starting point matters far less than the decision to begin and remain consistent.

A genuine financial cushion should generally exist before aggressive investing begins. Our complete emergency fund blueprint covers exactly this foundational protection, ensuring that an unexpected expense does not force premature withdrawal from a compounding investment account.

Quick Action Steps: Start Compounding This Month

Step 1: List any high-interest debt currently outstanding and prioritize eliminating it before increasing investment contributions significantly.

Step 2: Set up an automatic monthly transfer into an investment account, even starting with a modest, sustainable amount.

Step 3: Choose one passive income asset category — dividend stocks, real estate, or another option — to research and begin building this month.

Step 4: Commit to a minimum five-year evaluation period before judging whether your investment plan is “working,” since meaningful compounding results take time to become visible.

Step 5: Reduce your exposure to daily financial news and short-term market commentary, replacing it with a fixed quarterly portfolio review instead.

If you have not yet built a financial safety net to protect this process from interruption, the Consumer Financial Protection Bureau’s guidance on emergency savings offers a useful starting framework alongside our own emergency fund resources.

Frequently Asked Questions

How does compounding actually build wealth over time?

Compounding allows investment earnings to be reinvested, generating their own additional earnings on top of the original principal. This creates exponential rather than linear growth, where the rate of growth itself accelerates over time as the base of invested capital increases.

Why does compounding feel slow in the first few years?

Compounding is mathematically back-loaded, meaning the majority of visible, dramatic growth occurs in the later portion of an investment timeline rather than evenly throughout. The early years involve genuine growth that simply is not yet large enough to look visually significant, which is why this period requires patience rather than evidence of results.

Is it better to start investing early with small amounts or wait and invest larger amounts later?

Starting early with smaller, consistent amounts generally outperforms starting later with larger contributions, because compounding requires time to produce its most significant results. The total time invested often matters more than the total amount contributed when comparing long-term outcomes.

Should I pay off debt or start investing first?

High-interest debt should generally be prioritized before aggressive investing, since the same compounding mechanism that builds wealth in investments works against you when applied to debt. Eliminating high-interest obligations first removes a force actively working against your overall financial progress.

What is the biggest mistake people make with compounding?

The most common and costly mistake is interrupting the compounding process — withdrawing accumulated investments early, pausing contributions during difficult periods, or abandoning a plan during the slow, unimpressive early years right before significant growth would have become visible.

How do I transition from active income to passive income using compounding?

This transition typically involves reinvesting earnings from dividends, rental income, or business profits back into additional income-generating assets, rather than spending those earnings as they arrive. Over time, this reinvestment compounds the income-generating base itself, gradually reducing dependence on active work for income.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial or investment advice. Individual financial outcomes vary based on personal circumstances, risk tolerance, and market conditions. The Data Pips Team makes no guarantees regarding financial outcomes from applying the strategies described in this article. Consult a licensed financial advisor before making investment decisions.