The investment landscape in 2026 is no longer about just buying low and selling high. With shifting geopolitics, rising AI adoption, and increasing market volatility, investors need a more disciplined and sophisticated approach. But before we dive into opportunities, let’s address the most important part of investing that most people skip: not losing your money.

Table of Contents

1. A Reality Check for Every Investor

Whether you are a seasoned professional or a complete beginner, the first piece of advice is this: do your own research. Do not blindly follow this article or any post you see online. Markets change. If you are reading this months after publication, the entry points for specific stocks may have shifted significantly.

Investing without a setup and a strategy is a recipe for disaster. You might find yourself stuck in a loss for years simply because you bought at the peak without a plan — not because the underlying investment was bad, but because your timing and preparation were not.

If you are a beginner, learn first. Use educational resources, YouTube, and practice with a Demo Account before putting a single real dollar into the market. According to Investopedia, the most common mistake new investors make is entering the market before they understand the basics of risk management. Understanding before acting is not a weakness — it is the foundation of every successful investor.

![🖼️ [NEW IMAGE: Beginner investor studying charts with demo account open — learning before investing concept. AI Prompt: Young person at desk with two screens — one showing demo trading account, one showing educational content. Motivated, focused expression. Modern home office. Alt Text: Learn before you invest — demo account and education as foundation of smart investing]](https://datapips.net/wp-content/uploads/2026/04/young-beginner-investor-at-modern-home-office-desk-1024x576.jpeg)

2. The Anti-Gambler Strategy: Master Risk Management

If you throw money into the market without a plan, you are not an investor. You are a gambler. And the market has no mercy for gamblers — it systematically transfers their capital to those who are prepared.

To survive among institutional traders — the whales who move markets — you must master Risk Management.

Here is a simple but powerful formula. Suppose you have $5,000 to invest:

- Deploy: $2,000 — less than 50% of your capital at entry.

- Reserve: $3,000 — kept as backup, untouched.

Why? Because if the market drops after your entry, your reserve allows you to buy more at lower prices — a strategy called averaging down. If you go all-in at once and the market crashes, you are helpless. You have no ammunition left and no choice but to hold a losing position or sell at a loss.

This principle is supported by decades of institutional trading practice. As Charles Schwab outlines in their investor education resources: position sizing and capital reservation are the two most critical factors in long-term portfolio survival — not stock selection.

3. Learn the Concepts — There Are No Shortcuts

Spend three to four months back-testing any strategy before committing real capital. Whether it is Fundamental Analysis, Chart Patterns, or Price Action — verify that it works across different market conditions before you trust it with money that matters.

Remember the scale you are operating at. Large institutional players are protecting millions and billions. Your $10,000 or even $50,000 is statistically invisible to them. To win in this environment, you must learn to position yourself alongside the “operators” — the market makers and institutional flows — rather than against them.

The goal is not to outsmart institutions. The goal is to read what they are doing and align with it. That skill takes time to develop. There is no shortcut that bypasses the learning phase.

4. A Tale of Two Mindsets: The 1929 Lesson

History is one of the most powerful teachers available to any investor. The contrast between two types of people during the Great Depression of 1929 remains one of the most instructive stories in financial history.

One type was the wealthy show-off who put every penny into the market, chasing overnight riches. When the market crashed, he lost everything — not because investing was wrong, but because his approach was reckless and his position size was irresponsible.

The other type was Ronald Read — a gas station attendant and janitor who never earned a high salary, never had a prestigious degree, and never flaunted any wealth. He simply bought quality stocks and held them for decades without panic, without selling during downturns, and without chasing trends. When he passed away, the world was shocked: he had quietly accumulated a fortune of $8 million.

His story, documented by The Motley Fool, is one of the clearest real-world proofs that compounding, patience, and quality outperform speculation every time over a long enough horizon.

The lesson: Stock market success is not about looking rich today. It is about being wealthy when you are older and genuinely need it. It is about compounding, not gambling.

5. The Get Rich Quick Trap

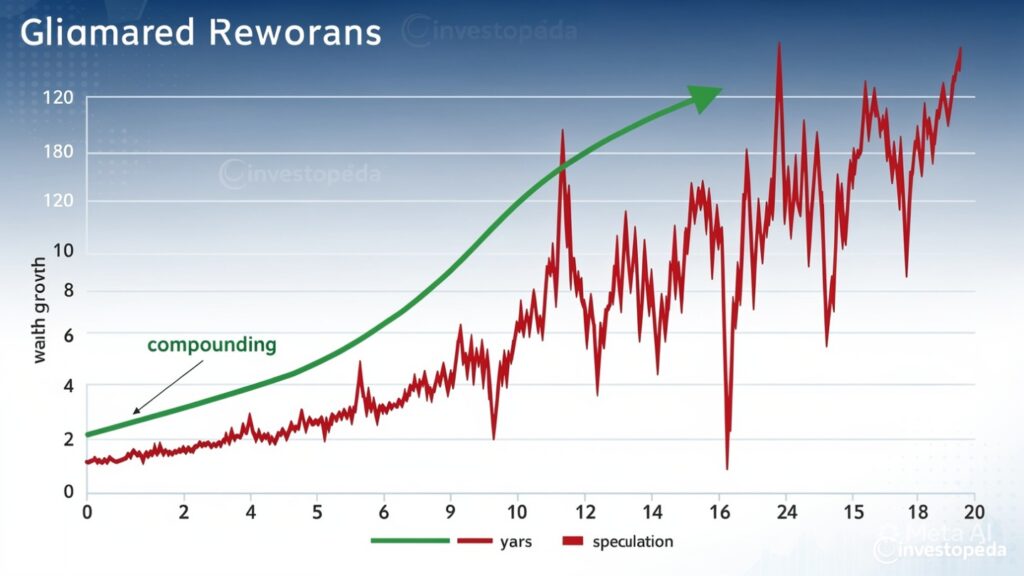

If you are looking to become a millionaire overnight, the stock market — or forex, or crypto — is not the vehicle for that. Meme coins exist. Lottery-style gains exist. But 95% of people who chase them lose their capital, their time, and sometimes their confidence permanently.

True wealth is built through compounding. It takes time, patience, and a long-term mindset. The mathematics are unambiguous: a consistent 12-15% annual return compounded over 20-30 years produces results that dwarf any lucky short-term gain.

As Warren Buffett has consistently demonstrated through Berkshire Hathaway’s letters to shareholders — the most reliable path to extraordinary wealth is ordinary discipline, applied for an extraordinary length of time.

6. 2026 Sectors Worth Watching — After You Do Your Research

Once you have mastered your entry approach, risk management, and back-testing — keep these sectors on your watchlist for 2026:

- The Digital Backbone: Companies like CDSL and BSE that act as the infrastructure of financial markets. As digital adoption grows, the infrastructure that supports it becomes increasingly valuable.

- Power and Connectivity: Leaders like Polycab India and Hindustan Copper that are essential for the data center and AI infrastructure boom. Physical infrastructure for digital growth is one of the clearest macro trends of this decade.

- Consumer Finance: Giants like Bajaj Finance that benefit from the growing middle class and increasing access to credit in emerging markets.

Important: These are not recommendations. They are sectors to research. Entry points, valuations, and market conditions change. Always verify current data before making any investment decision.

Frequently Asked Questions

Q: How much money do I need to start investing?

You can start with as little as $50 to $100 through fractional shares or index funds. The amount matters less than the habit of starting early and reinvesting consistently. What kills most beginners is waiting until they have “enough” — that moment rarely arrives on its own.

Q: What is the safest investment for beginners in 2026?

Low-cost index funds tracking broad markets — like S&P 500 ETFs — are consistently recommended for beginners by most financial educators. They provide instant diversification, low fees, and historically reliable long-term returns without requiring individual stock selection skills.

Q: How long should I back-test a strategy before using real money?

A minimum of 3 to 4 months across different market conditions — both trending and ranging. One hundred or more sample trades in back-testing gives you a statistically meaningful picture of how the strategy performs. Fewer samples produce unreliable conclusions.

Q: Is the stock market gambling?

Uninformed, emotionally-driven investing without risk management is functionally similar to gambling. Disciplined investing with proper position sizing, diversification, and a long-term horizon is mathematically different — it has a positive expected value over time. The difference is entirely in the approach, not the asset class.

Q: What was Ronald Read’s actual strategy?

Ronald Read bought shares in well-known, dividend-paying companies and held them for decades without selling during downturns. He reinvested dividends and lived modestly. His strategy was not sophisticated — it was consistent. That consistency, applied over a long enough period, produced an $8 million portfolio on a janitor’s salary.

Q: Should I invest in crypto in 2026?

Only with capital you can afford to lose entirely — and only after mastering risk management with more stable assets first. Crypto offers significant return potential but equally significant volatility and risk. It should be a small, informed allocation within a broader portfolio, never a primary investment vehicle for capital you cannot replace.

About the Author

Shurah Beel Hamid is a business enthusiast, active trader, and content creator who transformed his life by training his brain from an electrician’s mindset to an entrepreneur’s mindset. His expertise lies in practical brain training for entrepreneurship, trading psychology, compounding strategies, and elite mindset development. He shares his raw, unfiltered journey — from suicidal thoughts to strategic patience, from blowing trading accounts to consistent profitability — to provide actionable insights for those tired of theoretical advice and ready for real change. His writing combines hard-won experience, neuroscience-backed techniques, and relentless optimism.

Disclaimer: This article is for educational purposes only. Investing involves risk. Please consult with a financial advisor and perform your own due diligence. Markets are volatile and past performance is not indicative of future results.