We ran a simple experiment at Data Pips last year. We tracked two hypothetical portfolios over 20 years. Portfolio A earned 10% annually and the investor never touched it. Portfolio B earned 12% annually — objectively better performance — but the investor withdrew profits twice, panic-sold once, and switched strategies three times. The result? Portfolio A ended with $67,275 from a $10,000 start. Portfolio B ended with $31,058.

Read that again. The worse-performing portfolio produced more than double the wealth. Not because of better returns. Because the investor in Portfolio A did the one thing that 92% of investors psychologically cannot do: absolutely nothing.

This is what sabotaging compounding looks like. It doesn’t happen through bad investments or market crashes. It happens through tiny, invisible decisions that feel rational in the moment but systematically destroy the most powerful wealth-building force in existence. And the worst part? Most investors don’t even realize they’re doing it.

At Data Pips, we’ve spent years studying why intelligent people make self-destructive financial decisions. What we’ve found is uncomfortable: the enemy of compounding isn’t bad markets. It’s human behavior. And in this article, we’re going to expose every single pattern that’s quietly murdering your returns — so you can stop before it’s too late.

Table of Contents

The Math That Should Terrify Every Investor

Before we dissect the behavioral patterns, we need you to understand something about compounding that most people grasp intellectually but never feel emotionally. And that gap between understanding and feeling is exactly where the sabotage lives.

Compounding is exponential. Your brain thinks linearly.

Here’s what that means in real numbers. If you invest $10,000 at 10% annual return:

- After Year 1: $11,000 (gained $1,000)

- After Year 10: $25,937 (gained $15,937)

- After Year 20: $67,275 (gained $57,275)

- After Year 30: $174,494 (gained $164,494)

- After Year 40: $452,593 (gained $442,593)

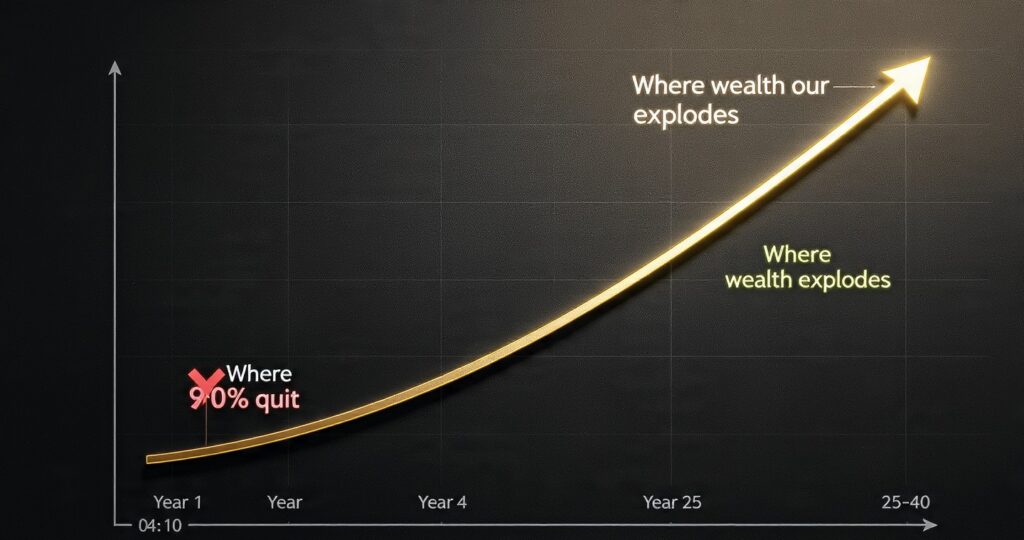

Look at the acceleration. In the first decade, you gained about $16K. In the last decade alone, you gained over $278K. Almost 63% of your total wealth was generated in the final 10 years of a 40-year journey.

This is the concept that Investopedia describes as “interest on interest” — and it’s the single most powerful force in personal finance. But here’s the problem: your brain can’t visualize exponential growth. It expects linear progress — equal gains every year. When the early years produce small, boring returns, your emotions scream that something is wrong. And that scream is where the sabotage begins.

Warren Buffett earned over 99% of his wealth after his 50th birthday. Not because he suddenly got smarter. Because compounding needs time — and he gave it the one thing most investors refuse to: uninterrupted decades.

As we broke down in our complete guide to compounding, the math is simple. The psychology is where everything falls apart.

Sabotage Pattern #1: Withdrawing Profits Too Early

This is the most common and most devastating form of compounding sabotage. You invest, it grows, and the moment you see a decent profit, you pull it out. Maybe you “reward yourself.” Maybe you move it to a “better opportunity.” Maybe you just feel nervous holding that much unrealized gain.

Whatever the reason, the math is merciless. Every dollar you withdraw doesn’t just cost you that dollar. It costs you everything that dollar would have become over the next 10, 20, 30 years.

Withdrawing $5,000 in profit might feel like taking $5,000. But at 10% compounding over 20 years, you actually took $33,637 from your future self. That $5,000 was a seed that would have grown into a tree. You ate the seed.

We’ve detailed this exact mistake in our article on common compounding mistakes. The pattern is always the same: withdraw early, feel smart temporarily, realize the cost years later when it’s too late to recover.

The Cure:

Create an absolute rule: compounding capital is untouchable for a minimum of 5 years. Not “unless I need it.” Not “unless a better opportunity comes.” Untouchable. Period. If you need liquidity, keep a separate emergency fund. Your compounding account is a time capsule that your future self will open.

Sabotage Pattern #2: The Strategy-Hopping Disease

New crypto fund promising 40% returns? Jump in. Friend made money on real estate? Switch to property. Some guru on YouTube says gold is about to explode? Liquidate everything and buy gold. Every time you switch strategies, you reset your compounding clock to zero.

According to the Dalbar Quantitative Analysis of Investor Behavior, the average equity fund investor earned 3.6% annually over 20 years — while the S&P 500 returned 7.5%. That gap didn’t come from bad fund selection. It came from investors jumping in and out of funds at exactly the wrong times. The market didn’t fail them. Their behavior did.

Strategy-hopping feels productive. It feels like you’re optimizing, adapting, being smart. In reality, you’re restarting a marathon at mile 1 every time you switch routes. Compounding rewards consistency over cleverness.

The Cure:

Pick one investment vehicle. One strategy. Give it a minimum of 36 months before you even consider changing. Not 36 days. Not 36 weeks. 36 months. If it underperforms the benchmark over three full years, then evaluate. Before that, your emotions are not data — they’re noise.

Sabotage Pattern #3: Panic Selling During Downturns

The market drops 30%. Your portfolio is bleeding red. Every headline screams disaster. Your brain — wired for survival, not wealth-building — fires every alarm it has. SELL. GET OUT. SAVE WHAT’S LEFT.

And so you sell. Right at the bottom. The exact worst moment. Then you watch from the sidelines as the market recovers without you. By the time you feel “safe” enough to re-enter, prices are higher than where you sold. You locked in a loss and missed the recovery. The compounding chain is broken.

This isn’t a rare mistake. It’s the default human response. J.P. Morgan’s research consistently shows that missing just the 10 best trading days over a 20-year period can cut your total returns by more than half. And those best days? They almost always occur within days of the worst days — right when panic sellers are sitting on the sidelines.

We explored this deeply in our article on compounding from our own experience. The most painful moments — when everything seemed lost — were exactly the moments that produced the highest future returns for those who stayed.

The Cure:

Before you invest a single dollar, write down this sentence and tape it to your monitor: “Market crashes are compounding events, not compounding endings.” Every major market downturn in history has been followed by recovery and new highs. The only people who permanently lost money were the ones who sold during the crash and never came back.

Sabotage Pattern #4: Obsessive Portfolio Checking

You check your portfolio 14 times a day. Every green candle makes you euphoric. Every red candle makes you anxious. By the end of the week, you’ve experienced 70 emotional swings — none of which changed your actual long-term outcome, but all of which degraded your decision-making quality.

Over-monitoring is the silent compounding killer that nobody talks about.

Here’s what the research shows: on any given day, the stock market has roughly a 53% chance of being positive and a 47% chance of being negative. Check daily, and you’ll see red nearly half the time. Check monthly, and the positivity rate jumps to about 63%. Check annually, and it’s around 75%. The less frequently you look, the better your investment appears — not because the returns changed, but because your emotional experience changed.

And emotional experience drives behavior. See red too often, and your brain starts building a case for selling. See green consistently, and your brain reinforces staying. Same investment. Different observation frequency. Completely different outcome.

The Cure:

Set a schedule. Check your long-term compounding portfolio once a month. Not once a day. Not once a week. Once a month. On the same date. For 15 minutes. Then close it and go live your life. Your money doesn’t need your attention. It needs your absence.

Sabotage Pattern #5: Chasing “Better” Returns Instead of Protecting Existing Ones

Your portfolio is compounding at 9% annually. Boring but reliable. Then you hear about an opportunity promising 25%. Your brain does the quick math — 25 is obviously better than 9 — and you move your capital.

What your brain didn’t calculate: the 25% opportunity has a 40% chance of losing 50% of your capital. The expected value, adjusted for risk, is actually lower than your boring 9%. But expected value isn’t exciting. Big numbers are exciting. And excitement is the enemy of compounding.

We call this “return chasing” and it’s one of the most researched phenomena in behavioral finance. Investors consistently move money into whatever performed best recently — arriving just as the cycle peaks and leaving just as their original investment starts its next growth phase.

The Berkshire Hathaway annual letters repeatedly emphasize this principle. Buffett has said he’d rather earn 12% consistently for 30 years than 30% for one year followed by chaos. Compounding doesn’t reward the highest return. It rewards the most consistent one.

We covered the mechanics of this in our article on consistent compounding returns — and the data is conclusive: consistency beats brilliance every single time over a multi-decade horizon.

The Cure:

Before chasing any “better” opportunity, ask three questions:

- What is the realistic downside — not the best-case scenario?

- What will this switch cost me in compounding continuity?

- Am I moving toward a strategy, or away from boredom?

If you’re moving away from boredom, sit down. Boredom is the price of compounding. Pay it gladly.

Sabotage Pattern #6: Emotional Reinvestment Timing

Market drops? “I’ll wait until it stabilizes.” Market rises? “I’ll wait for a pullback.” The market goes sideways? “I’ll wait for direction.” The result? You wait forever. Your cash sits earning nothing while compounding time — the most irreplaceable resource — evaporates.

This is different from panic selling. This is the investor who has cash ready to invest but keeps waiting for the “right time.” The right time was yesterday. The second-best time is today. The worst time is “when I feel comfortable” — because comfort in investing usually arrives precisely when opportunity has already left.

Data from multiple studies shows that dollar-cost averaging — investing a fixed amount at regular intervals regardless of market conditions — outperforms waiting for the “perfect entry” in over 70% of historical scenarios. Not because it’s smarter. Because it removes the emotion that causes timing paralysis.

The Cure:

Automate your investing. Set a fixed amount to invest on a fixed date every month. Rain or shine. Bull or bear. Good news or bad. Remove yourself from the equation. Your investment schedule should be as emotionless as your electricity bill — it just happens.

Sabotage Pattern #7: Treating Compounding Like a Sprint

This is the most psychologically devastating pattern because it kills motivation before compounding even has a chance to work. You invest $10,000. After one year, it’s worth $11,000. One thousand dollars of profit. Your brain screams: “That’s it? I waited an entire year for this?”

And so you quit. Or you switch to something “faster.” Or you start taking unnecessary risks to speed things up. All because you couldn’t tolerate the early-stage boredom of compounding — the phase where the numbers seem insultingly small compared to the patience required.

But here’s what you failed to see: that $1,000 wasn’t the prize. It was the foundation. In Year 20, that same capital generates $6,116 in a single year — from the same 10% rate. In Year 30, it generates $15,863. Compounding pays the most to those who expect the least in the beginning.

This connects directly to what we teach in our business compounding strategy guide: compounding isn’t just a financial tool. It’s a philosophy. Whether you’re compounding money, skills, or reputation, the early phase always feels disproportionately slow compared to the result it eventually delivers.

The Cure:

Change what you measure. Instead of checking your total profit (which will feel depressingly small early on), track your compounding rate and your compounding streak — how many consecutive months you’ve invested without interruption. The streak IS the success. The dollars are a lagging indicator.

The Behavioral Firewall: A System to Protect Yourself from Yourself

Knowing these seven patterns isn’t enough. You knew smoking was bad before you quit (if you did). Knowledge doesn’t change behavior. Systems change behavior. Here’s the system our team recommends to build a behavioral firewall around your compounding:

- Separate your accounts physically. Compounding capital goes in a separate account at a different institution than your spending money. Out of sight, out of mind, out of temptation.

- Automate contributions. Fixed amount. Fixed date. No decision required. The best investment plan is one that runs without your emotional involvement.

- Delete portfolio apps from your phone. Check your compounding portfolio on a laptop, once a month, on a scheduled date. Never on your phone. Phones are emotional triggers.

- Write a “crisis letter” to yourself. While you’re calm and rational, write a letter explaining why you should NOT sell during a market crash. Seal it. When the next crash comes (and it will), open and read it before making any decision.

- Find an accountability partner. Someone who will talk you off the ledge when your brain screams “SELL EVERYTHING.” This person doesn’t need to be a financial expert. They need to be calm when you’re not.

“The investor’s chief problem — and even his worst enemy — is likely to be himself.” — Benjamin Graham, The Intelligent Investor

⚡ Quick Action Steps: Stop Sabotaging Your Compounding Today

- This week: Open a separate investment account at a different bank than your daily spending account. Label it “Do Not Touch Until [Year 10 years from now].” Even if you start with $100, the separation is what matters.

- Today: Set up an automatic monthly transfer to that account. Even $50/month. The automation removes your emotions from the equation permanently.

- Right now: Delete all portfolio-tracking apps from your phone. Move to monthly desktop-only check-ins. Your compounding doesn’t need daily attention — it needs daily neglect.

- This weekend: Write your “crisis letter.” Explain to your future panicked self why selling during a downturn is the single worst financial decision they can make. Be specific. Be harsh. Your future self needs the tough love.

- Before month’s end: Calculate your “compounding streak” — how many consecutive months you’ve invested without withdrawing. If you don’t have one, today is month 1. Protect that streak like your financial life depends on it — because it does.

The Uncomfortable Question You Need to Answer

We’re going to leave you with a question that should keep you up tonight — not from anxiety, but from self-awareness:

How many times have you already sabotaged your own compounding?

Think back. The investment you sold too early because it “wasn’t growing fast enough.” The strategy you abandoned after six months because someone showed you something shinier. The portfolio you liquidated during COVID because the headlines terrified you — then watched it recover 100% without you in it.

Every one of those moments was a compounding chain being broken. And the cruel truth about broken compounding chains is that you never see what you lost. You only see what you walked away with. The invisible cost — the decades of growth you forfeited — never appears on any statement.

That’s what makes this sabotage so insidious. It doesn’t feel like a mistake when you’re making it. It feels like a decision. A smart one, even. The pain only arrives years later, when you calculate what your portfolio would have been worth if you’d simply done nothing.

“Compounding doesn’t reward the smartest investor. It rewards the one who got out of their own way the longest.” — Data Pips Team

Frequently Asked Questions

1. What does it mean to “sabotage compounding”?

Sabotaging compounding means taking actions that interrupt the continuous, uninterrupted growth of your investments — even when those actions feel logical at the time. This includes withdrawing profits prematurely, panic selling during market downturns, switching investment strategies too frequently, and over-monitoring your portfolio. Each interruption resets your compounding clock, and the lost time can never be recovered because time is compounding’s essential ingredient.

2. Why do smart people still sabotage their compounding?

Because intelligence and emotional discipline are completely different capabilities. Smart people can explain compounding on a whiteboard but still panic sell during a 30% market drop. The human brain is wired for short-term survival, not long-term wealth optimization. Seeing a portfolio drop from $100K to $70K triggers the same neurological alarm as a physical threat — and no amount of intellectual understanding can override that alarm without systems and behavioral firewalls in place.

3. What’s the single worst way investors sabotage their compounding?

Panic selling during market downturns — and it’s not even close. Research consistently shows that investors who sell during crashes and wait for “stability” before re-entering miss the majority of recovery gains. The best market days almost always cluster within days of the worst market days. By selling at the bottom and buying back near the top, you crystallize losses and miss recoveries. One panic sell can cost you a decade of compounding progress.

4. How often should I check my long-term investment portfolio?

Once a month. Maximum. And ideally on a desktop or laptop, not your phone. Every additional check increases your emotional exposure without providing actionable information. Daily checking means experiencing negative returns roughly 47% of the time. Monthly checking drops that to roughly 37%. Annually, you see positive returns about 75% of the time. Less observation = better emotional experience = fewer self-destructive decisions.

5. Is it ever okay to withdraw from a compounding portfolio?

Only in genuine emergencies that threaten your survival — medical crises, housing security, critical family situations. “I found a better opportunity” is not an emergency. “I want to upgrade my car” is not an emergency. “The market is scary right now” is definitely not an emergency. Build a separate emergency fund specifically so you never have to touch your compounding capital. The two should exist in completely different mental and physical accounts.

6. What if my investment strategy actually is bad — shouldn’t I change it?

Yes — but only after giving it enough time to prove itself. Our rule is 36 months minimum before evaluating a strategy change. Markets cycle. Strategies have good years and bad years. Judging a long-term strategy on 6-12 months of data is like judging a farmer’s skill based on one season’s weather. If after three full years your strategy consistently underperforms reasonable benchmarks, pivot deliberately — not emotionally.

7. How much does missing the best market days actually cost?

The numbers are staggering. J.P. Morgan’s research shows that if you invested $10,000 in the S&P 500 from 2003-2022 and stayed invested, you’d have $64,844. Miss the 10 best days, and you’d have $29,708. Miss the 20 best days: $17,826. Miss the 30 best days: $11,701. Missing just 30 days out of roughly 5,000 trading days cost you over 80% of your returns. And those best days? They occurred right after the worst days — precisely when panic sellers were sitting in cash.

Conclusion: The Hardest Part of Compounding Is Doing Nothing

We’ve just shown you seven distinct ways investors sabotage their own compounding — and every single one has the same root cause: the inability to sit still while the math works silently in the background.

Compounding doesn’t need your genius. It doesn’t need your market timing. It doesn’t need your constant attention. It needs one thing from you that is simultaneously the simplest and hardest thing in all of finance: sustained, disciplined, almost aggressive inaction.

At Data Pips, we’ve studied compounding across trading, business, and personal finance. The principle is always the same. The people who win aren’t the ones with the best entries or the cleverest strategies. They’re the ones who protect their compounding chain from their own behavior.

Build the behavioral firewall. Automate the process. Write the crisis letter. Delete the apps. Check monthly, not hourly. And every time your brain screams at you to do something — to sell, to switch, to “optimize” — remind yourself that the most profitable action in compounding is the one you didn’t take.

How many of these seven sabotage patterns did you recognize in yourself? Be honest in the comments — our team reads every single one, and self-awareness is the first step to stopping the damage before another compounding cycle is lost.

Disclaimer: This article is for educational and informational purposes only. It does not constitute financial advice, investment advice, or any other type of professional advice. All investments carry risk, including the potential loss of principal. Past performance does not guarantee future results. The examples, calculations, and scenarios described are illustrative and may not reflect actual market conditions or individual outcomes. Always consult a licensed financial advisor before making investment decisions. Data Pips is not a registered investment advisor and does not manage client funds.