- Burning personal savings during the learning phase of trading creates psychological trauma that makes future discipline significantly harder to build.

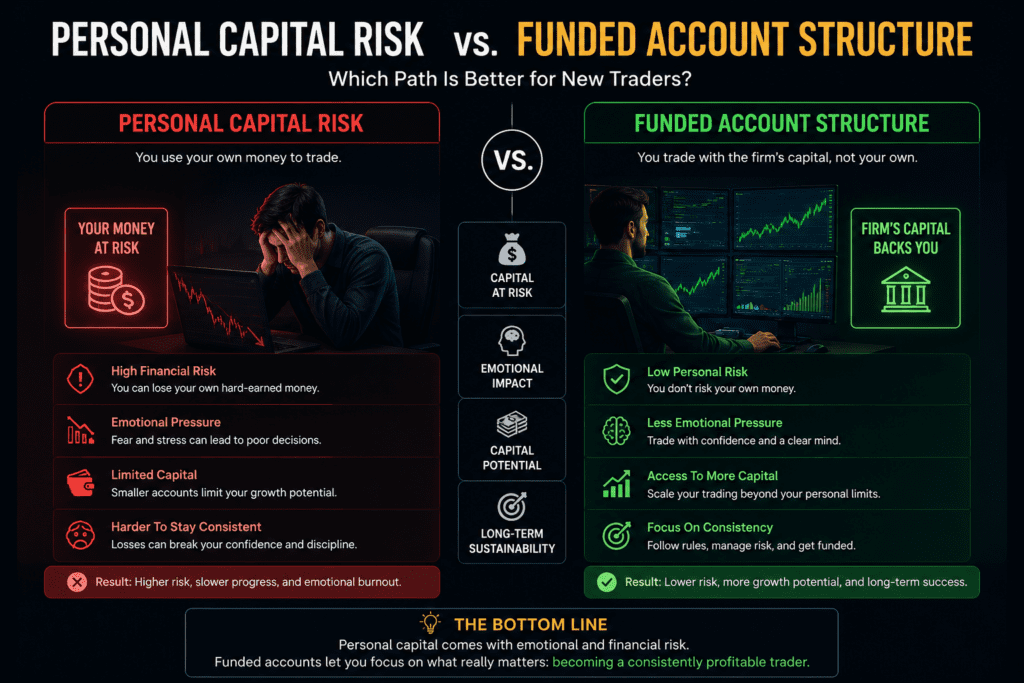

- A funded account through a prop firm challenge limits personal financial risk to an evaluation fee, while still providing real capital and real consequences to learn from.

- An unmanaged emotion is more dangerous to a trading account than any single bad trade.

- Trading is closer to 10% strategy and 90% psychology — most of the actual work happens long after the chart analysis is finished.

Trading gets marketed constantly as easy money. After years inside real forex and gold markets, the more honest description is the opposite: trading is one of the hardest ways to make money that looks easy from the outside. For many traders, the journey toward consistency is not a smooth, overnight transition — it is a long, often expensive battle against habits and emotions that no amount of technical knowledge fixes on its own.

The specific mistake that extends this battle far longer than necessary is a common one: learning to trade using personal savings, absorbing real financial pain during the exact period when mistakes are most frequent and least informed. This article explains why that approach causes damage far beyond the dollar amount lost, and why a fundamentally different starting structure — a funded account — protects both capital and the psychological foundation a trader actually needs to develop real discipline.

This guide from the Data Pips Team is built on hard, real lessons from years of trading gold and forex, not theoretical advice from someone who has never felt the weight of a losing streak.

The Real Cost of Learning to Trade With Personal Savings

The most expensive mistake in any new trader’s journey is rarely a single bad trade. It is the cumulative psychological damage of repeatedly losing personal, hard-earned savings during a learning period defined by inexperience and inconsistent discipline.

Money lost while genuinely learning a skill is different in character from money lost through a calculated, informed decision. Early-stage trading losses happen while the trader is still building fundamental pattern recognition, risk management habits, and emotional regulation — meaning the losses are disproportionately caused by inexperience rather than by genuinely bad probability decisions. When that lost money is personal savings, the financial pain compounds with a deeper emotional toll: the awareness that years of saving disappeared during a period of trial and error that could have been structured very differently.

This kind of accumulated financial and emotional weight does not stay contained to a trading account. It frequently affects relationships, sleep, and overall mental wellbeing, creating exactly the kind of chronic stress that further impairs the calm decision-making trading actually requires.

The Three Pillars Most New Traders Ignore

Chasing a perfect strategy distracts from the three elements that actually determine long-term trading outcomes: risk management, psychology, and emotional control. Technical strategy knowledge is necessary but nowhere near sufficient on its own.

Trading leans far more heavily toward psychology than most beginners expect — closer to a 10% strategy, 90% psychology split in terms of what actually determines results over time. Investopedia’s research on trading psychology reinforces this directly, confirming that a trader’s beliefs and emotional discipline consistently outweigh raw technical analysis skill in determining long-term outcomes.

The turning point for most traders who eventually find consistency is not a better strategy. It is the moment they stop fighting the market and start addressing their own ego, accepting losses without denial, and implementing genuinely strict risk management instead of treating it as an optional add-on to an otherwise exciting trading plan.

“An unmanaged emotion is more dangerous to your account than any single bad trade you will ever take.”

— Data Pips Team

Emotions: The Destroyer of Wealth and Relationships

Unmanaged emotion in trading does not just damage a bank account. Left unaddressed long enough, it damages relationships, sleep, and overall quality of life. The specific trap repeats predictably: a loss triggers a desire for revenge, taken out on the very next trade through oversized risk, while a win triggers overconfidence that leads to the same oversized risk from the opposite direction.

The fix is not eliminating emotion, which is not realistically possible. It is learning to treat a loss as a business expense rather than a personal failure — a reframe that sounds simple but takes genuine, sustained practice to internalize under real financial pressure. Our complete guide on treating trading as a business rather than a lottery expands on exactly this reframe in significant depth.

Why a Funded Account Changes the Entire Equation

If there is one structural decision that could meaningfully shorten the painful, expensive early years most traders go through, it is this: use a funded account through a proprietary trading firm challenge instead of risking personal savings directly during the learning phase.

The logic is straightforward. A funded account challenge typically requires a modest evaluation fee rather than full personal capital. This limits the maximum personal financial risk to that fee, while still providing access to meaningful trading capital and the genuine psychological pressure of real, consequential decision-making — the exact pressure that demo accounts fail to replicate convincingly.

| Factor | Personal Capital | Funded Account |

|---|---|---|

| Personal financial risk | Full amount of savings deployed | Limited to the evaluation fee |

| Psychological pressure | High, tied directly to survival needs | Present, but not tied to personal bills |

| Learning focus | Often clouded by fear of ruin | Strategy, discipline, professional structure |

| Capital access | Limited to personal savings | Significant capital after passing evaluation |

The principle behind this is direct: if a trader cannot pass a modest funded account challenge, they genuinely have no business risking that same amount of their own personal capital either. The challenge functions as a real-stakes filter, without the irreversible cost of burning through personal savings to discover the same lesson.

The Founder’s Real Lesson: Mastery After the Reset

The shift that actually changed long-term trading outcomes was never a new indicator or a more sophisticated strategy. It was the decision to stop fighting the market’s unpredictability and start addressing personal ego and emotional reaction instead. Accepting losses without denial, applying genuinely strict risk management, and following a structured methodology based on Smart Money Concepts — including Order Blocks and Fair Value Gaps — replaced years of searching for a perfect entry signal that never actually existed.

The mathematical shift mattered as much as the psychological one. Aiming for strong risk-to-reward ratios on every setup, rather than trying to be right on every single trade, meant that consistent profitability did not require a high win rate. It required ensuring that wins were meaningfully larger than losses, every time, without exception.

During the rebuilding phase after years of inconsistent results, a specific habit made the biggest difference: pausing before every trade to ask two direct questions — is this a genuine, valid setup, or am I simply bored and looking for action? Is this disciplined execution, or is this revenge trading disguised as conviction? That brief moment of honest self-questioning, repeated consistently before every entry, filtered out a significant share of the emotionally driven trades that had previously caused the most damage. The technical knowledge had been present for years. The discipline to apply it consistently was the part that finally changed the results.

Risk-to-Reward Over Win Rate

One of the most counterintuitive lessons in trading is that being right most of the time matters less than most beginners assume. A trader can be wrong on the majority of individual trades and still be highly profitable overall, as long as the wins are significantly larger than the losses on average.

Investopedia’s explanation of risk-reward ratio confirms why targeting ratios well above 1:1 — often 1:3 or higher — fundamentally changes what win rate is actually required for long-term profitability. This mathematical reality removes much of the pressure to be “right” on every trade, replacing it with the more achievable goal of consistently letting winners run further than losers are allowed to cut.

What Nobody Tells You About Funded Accounts and Trading Psychology

1. A funded account does not eliminate emotional pressure — it changes its source. Passing a prop firm evaluation and trading real allocated capital still carries genuine psychological weight, including specific rules around drawdown limits and profit targets. The pressure is real, but it is not tied directly to whether personal bills get paid, which is precisely the distinction that protects mental health during the learning process.

2. The “six years of losing” pattern is common, but not inevitable. A prolonged losing period frequently happens specifically because risk management and psychology get treated as secondary to strategy. Traders who prioritize these two elements from the beginning, rather than discovering their importance only after years of losses, often compress that painful learning curve significantly.

3. Financial stress directly impairs the exact skills trading requires. The American Psychological Association’s research on stress and the body confirms that chronic stress measurably impairs cognitive function, including the patience and emotional regulation that disciplined trading depends on. This creates a vicious cycle when personal savings are at risk — the financial pressure itself degrades the decision-making needed to trade well.

4. A funded account challenge is not a shortcut around discipline. It is a structural tool that limits financial downside while the discipline itself is still being built through genuine practice, journaling, and consistent rule-following. Without that underlying discipline work, a funded account simply delays the same lessons rather than replacing the need to learn them.

5. Building income outside of trading reduces pressure on trading capital regardless of account type. Our guide on building multiple income streams without quitting your job covers a complementary strategy — financial stability from outside sources further reduces the temptation to trade desperately, whether the capital being traded is personal or allocated through a funded account.

It’s a Marathon, Not a Sprint

If a prolonged losing period feels familiar right now, the path forward is not abandoning trading entirely. It is honestly identifying what specifically is not working and changing the structural approach, rather than continuing to repeat the same pattern with mild variations. Protecting personal savings through a funded account structure, while simultaneously building genuine emotional discipline through journaling and mechanical execution, addresses both halves of the problem simultaneously rather than just one. Our guide on building mechanical discipline covers exactly this kind of structured execution in significant practical detail.

The market has enough opportunity for everyone who shows up with genuine discipline. The real question for most traders has never been whether the opportunity exists — it has always been whether they have the structure in place to actually capture it without destroying themselves financially and emotionally in the process.

Quick Action Steps: Protect Your Capital and Your Mind This Week

Step 1: If you are currently learning to trade with personal savings, research funded account or prop firm evaluation options that limit your personal risk to a fixed fee.

Step 2: Write down your current risk-to-reward target for trades, and evaluate honestly whether you are aiming for ratios that allow profitability without requiring a high win rate.

Step 3: Before your next trade, practice the two-question pause: is this a genuine setup, or am I bored? Is this discipline, or is this revenge trading?

Step 4: Reframe your next loss deliberately as a business expense rather than a personal failure, and track how that reframe affects your next decision.

Step 5: If financial pressure outside of trading is influencing your decisions, consider building a secondary income stream to reduce that pressure regardless of which account type you trade.

For the broader framework on why even smart, capable traders fail their first serious attempt, read our complete breakdown here.

Frequently Asked Questions

What is a funded trading account?

A funded trading account is capital provided by a proprietary trading firm after a trader passes an evaluation challenge, typically involving a modest upfront fee. This limits personal financial risk to that fee while granting access to significant trading capital under specific rules and profit-sharing arrangements.

Is it better to learn trading with a small personal account or a funded account challenge?

A funded account challenge generally limits personal financial risk more effectively than trading directly with personal savings during the learning phase, since the maximum loss is typically capped at the evaluation fee. This structure can reduce the psychological trauma associated with repeatedly losing personal savings while still learning fundamental skills.

Why is trading psychology more important than strategy?

A technically sound strategy still requires consistent, disciplined execution to be profitable. Without psychological control over fear, ego, and impatience, even an excellent strategy gets abandoned, oversized, or executed inconsistently, which is why beliefs and emotional discipline consistently outweigh raw technical analysis skill in long-term outcomes.

What risk-to-reward ratio should I aim for in trading?

Many disciplined traders aim for risk-to-reward ratios of 1:3 or higher, which allows for overall profitability even with a win rate below 50%. This shifts the focus from being right on every individual trade toward consistently letting winning trades run further than losing trades are allowed to extend.

How long does it typically take to become a consistently disciplined trader?

There is no universal timeline, and many traders go through an extended period of inconsistent results before genuine discipline develops. Prioritizing risk management and psychological discipline from the beginning, rather than treating them as secondary to strategy, can meaningfully shorten this learning period for some traders.

Does a funded account remove all emotional pressure from trading?

No. Funded accounts still carry genuine psychological pressure related to drawdown limits and performance rules, but that pressure is not directly tied to personal bills or savings. This distinction tends to make emotional regulation somewhat more manageable, though it does not eliminate the need to build real trading discipline.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial or trading advice. Trading forex, gold, and other leveraged instruments carries substantial risk of loss and is not suitable for all investors. Funded account and proprietary trading firm structures vary significantly by provider, and individuals should conduct thorough independent research before participating in any evaluation program. The Data Pips Team makes no guarantees regarding trading outcomes from applying the strategies described in this article. Always consult a licensed financial professional before making trading decisions.