Personal finance rules are not just about saving money, cutting coffee, or making a monthly budget that you forget after three days.

Look, I learned money the hard way.

I didn’t learn personal finance sitting comfortably in a classroom. I started my journey in 2018 when I was in 10th class. I left school, worked as an electrician and plumber for almost three years, and carried tools before I ever carried a proper financial plan.

Then came family pressure. Relatives’ taunts. Mental stress. Because my father was a government teacher, people expected a certain path from me. When I didn’t follow that path, the words hurt more than the work.

Honestly, there were moments where life felt too heavy. I went through dark mental phases that I don’t say proudly, but I say honestly because money pressure is real. Later, I worked in AC repair, entered trading through binary options, moved into forex, bought funded accounts, blew accounts, moved to Saudi Arabia, started a T-shirt business targeting expats, and slowly understood one thing:

Money is not only about earning more. Money is about awareness, leverage, discipline, and not trying to look rich before becoming financially strong.

Here’s the thing most people miss.

Rich people don’t think, “I need more money first, then I will build something.” They thi, “How can I use knowledge, systems, networks, investors, scholarships, credit, or other people’s resources safely to create value?”

Middle-class people often spend money to look rich. Rich people quietly use deals, leverage, and long-term thinking to actually build wealth.

This article is not theory. These are the personal finance rules I learned through mistakes, trading losses, small businesses, survival pressure, and painful self-awareness.

If you’re starting from zero, this is for you.

Table of Contents

What Are Personal Finance Rules?

Personal finance rules are the principles that control how you earn, spend, save, invest, borrow, and protect your money.

But I want to make this simple.

Personal finance is not about becoming cheap. It is not about living a sad life and never enjoying anything. It is about becoming aware enough that money stops controlling your mind.

When I was working as an electrician and plumber, I thought money was only income. If I earned more, I would be okay.

Then I entered trading. I saw people make money fast and lose it faster. I bought funded accounts and blew them because my risk management was weak. That was the first time I understood:

If your personal finance is weak, more income only gives you a bigger way to make bigger mistakes.

A person earning $500 can be financially healthier than someone earning $5,000 if the first person has discipline and the second person has ego.

The Real Goal of Personal Finance

The real goal is not just to have money.

The real goal is to build:

- Awareness — knowing where your money goes

- Control — spending intentionally, not emotionally

- Security — having emergency savings

- Growth — investing in skills and assets

- Freedom — not being trapped by bills, debt, or pressure

According to the Consumer Financial Protection Bureau, budgeting helps people understand income, expenses, and financial decisions clearly. I agree with that, but I would say it even more directly:

If you don’t track your money, your money will disappear quietly.

Rule 1: Financial Awareness Is the Light

Let me give you a simple example.

Imagine there is a mosquito in your room. If the light is on, you can see it. You can follow it. You can kill it.

But if the room is dark, even a tiny mosquito becomes a big problem.

That is exactly how money problems work.

The biggest financial problem is not always the biggest bill. The biggest problem is the one you cannot see.

Maybe it is small daily spending. Maybe it is unnecessary subscriptions. Maybe it is emotional shopping. Maybe it is trading revenge entries. Maybe it is lending money to people who never return it. Maybe it is lifestyle inflation.

Awareness is the light. Without awareness, even a small money leak can destroy your progress.

My Personal Example: I Was Losing Money Without Seeing It

When I started trading, I thought my problem was strategy.

I kept changing indicators, setups, platforms, and mentors. But when I finally reviewed my behavior honestly, I realized the real issue was not the strategy.

It was me.

I was risking too much. I was taking trades when I was emotionally disturbed. I was trying to recover losses quickly. I was treating funded accounts like opportunities to become rich fast instead of treating them like risk-controlled businesses.

The mosquito was not the market.

The mosquito was my lack of awareness.

How to Build Financial Awareness

Start with a simple weekly money check.

Every Sunday, write down:

- Total income received this week

- Total money spent this week

- Biggest unnecessary expense

- Debt payments made

- Amount saved

- Amount invested in skills or assets

- One money mistake to avoid next week

You don’t need a complicated spreadsheet at the start. Use a notebook, Google Sheets, or any budgeting app.

Pro Tip: Don’t judge yourself in the first month. Just observe. Seeing the truth is step one. Fighting comes later.

Rule 2: Rich People Use Leverage Carefully

This is one of the biggest differences I noticed between ordinary money thinking and wealthy money thinking.

Most beginners think:

“I don’t have money, so I can’t start.”

But wealthy people often think:

“What resource can I leverage without destroying myself?”

Leverage does not only mean debt. It can mean using other people’s money, other people’s audience, scholarships, partnerships, tools, systems, or knowledge.

But listen carefully.

Leverage is powerful, but it is dangerous if you use it without skill.

Good Leverage vs. Bad Leverage

Good leverage helps you grow with controlled risk.

Bad leverage makes you look smart for a short time and then destroys you when reality hits.

Examples of Good Leverage

- Using a scholarship instead of paying full university fees

- Starting a business with pre-orders before buying large inventory

- Partnering with someone who already has an audience

- Using business credit only when cash flow can repay it

- Using tools that save time and increase income

- Learning from mentors instead of repeating expensive mistakes

Examples of Bad Leverage

- Taking high-interest debt to look rich

- Using trading leverage without stop-loss discipline

- Borrowing money for a business you don’t understand

- Buying luxury items on installments

- Using investor money without a clear repayment or profit plan

The U.S. Small Business Administration provides information about funding options for businesses, but even business funding requires planning, documents, and repayment ability.

That is the part beginners ignore.

Rich people don’t just take money. They build systems that can handle money.

My Saudi Arabia T-Shirt Business Lesson

When I moved to Saudi Arabia, I started thinking about expats as a target market. T-shirts looked simple from outside, but the real game was not just printing shirts.

The real questions were:

- Who is the exact customer?

- What design do expats emotionally connect with?

- How much inventory should I hold?

- Can I test demand before spending too much?

- Can I use social media instead of expensive marketing?

That business taught me a personal finance rule I will never forget:

Don’t use money to cover lack of clarity. Get clarity first, then use money.

If I had blindly spent big money on stock, I could have been stuck with dead inventory. Testing small was leverage. Awareness was protection.

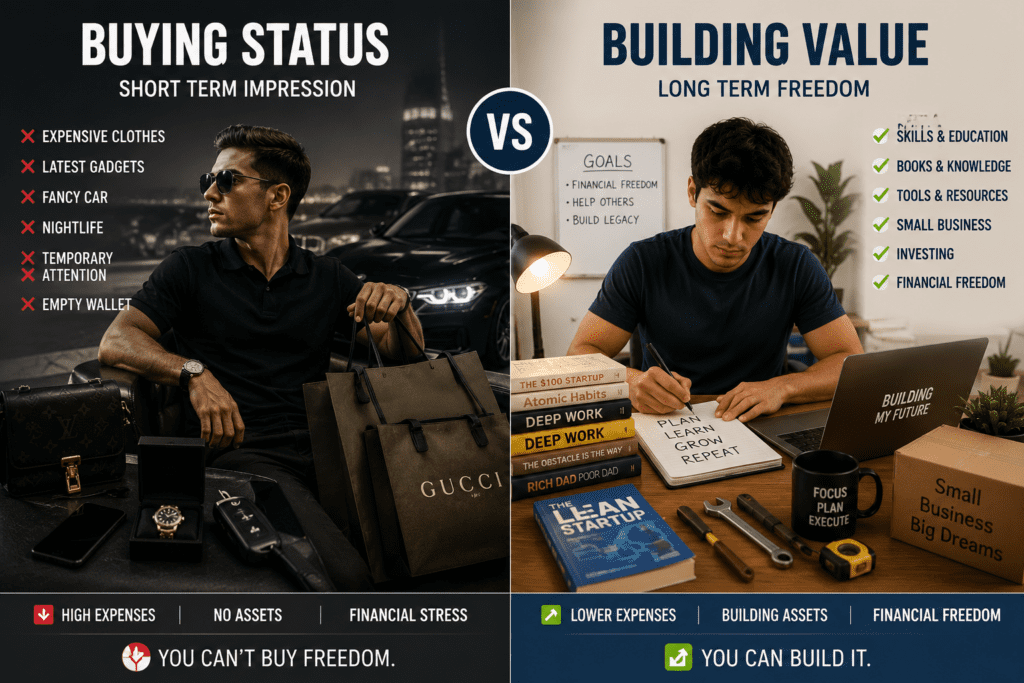

Rule 3: Stop Spending to Look Rich

Honestly, this rule hurts because many of us fall into this trap.

Middle-class people often spend money to prove they are doing well.

Expensive phone. Branded clothes. Bike or car payments. Fancy dinners. Social media lifestyle. Things bought not because they are needed, but because they send a message.

But here’s the thing:

If you need to spend money to look rich, you are probably moving away from becoming rich.

Rich people can spend on luxury too, of course. But smart wealthy people usually care more about value than appearance.

They ask:

- Is this the best deal?

- Does this improve my life or income?

- Is this an asset or just ego?

- Can I get the same result cheaper?

- Will this matter after six months?

Spend on Experiences, Skills, and Tools

One thing I learned slowly is that not all spending is bad.

Some spending makes you weaker. Some spending makes you stronger.

Buying something only to impress people usually makes you weaker financially.

But spending on a tool, skill, course, book, business test, health, or valuable experience can make you stronger.

When I worked in AC repair, better tools helped me work faster and more professionally. That was not waste. That was productive spending.

When I studied trading psychology after blowing accounts, that was painful but useful. The loss became tuition if I learned from it.

Personal Insight: Before buying anything expensive, I ask myself: “Is this building my future or feeding my ego?” That one question saves a lot of money.

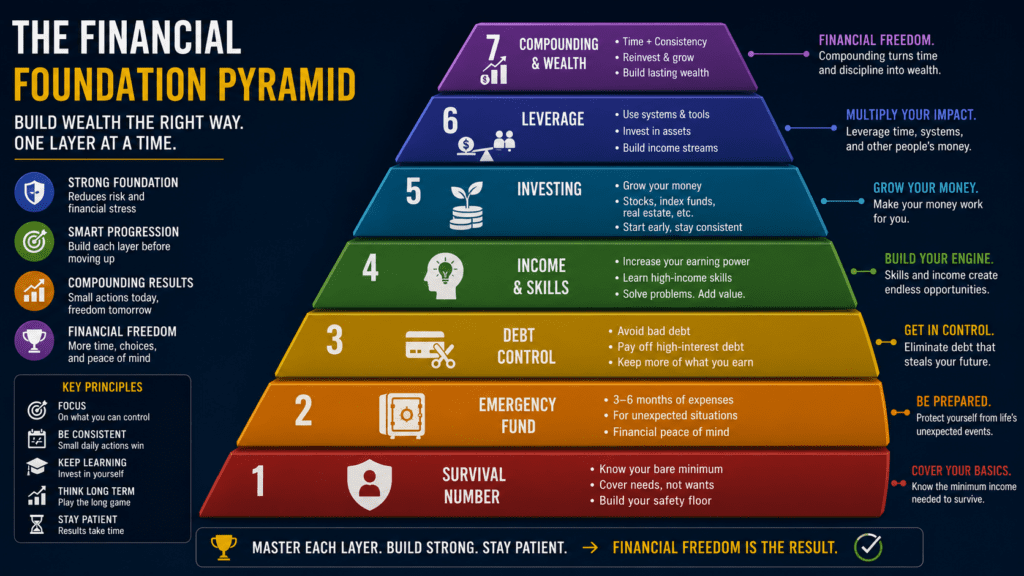

Rule 4: Build Your Financial Foundation First

Many people want investing, trading, crypto, forex, gold, stocks, or business before they even understand their monthly expenses.

I understand that mindset because I had it too.

When you are under pressure, you want a fast escape. Trading looks like escape. Business looks like escape. A funded account looks like escape.

But if your foundation is weak, opportunity becomes pressure.

The Financial Foundation Has 4 Parts

- Survival number — How much do you need monthly to survive?

- Emergency fund — At least 3-6 months of basic expenses if possible

- Debt control — Avoid high-interest debt and emotional borrowing

- Income skill — One skill that can reliably bring money

Your survival number is powerful.

If you need $500 per month to survive, then your first personal finance goal is not becoming a millionaire. Your first goal is to protect that $500/month lifestyle for a few months.

That gives your brain peace.

When your brain has peace, you make better decisions.

Why Emergency Funds Matter

An emergency fund is not exciting. It doesn’t make you look successful. Nobody claps for you because you saved rent money.

But it protects your dignity.

It stops you from taking desperate loans. It stops you from accepting bad deals. It gives you time to think.

In trading, we say protect capital. In life, emergency fund is your personal capital protection.

You can learn more about saving and budgeting basics from the CFPB budgeting resources.

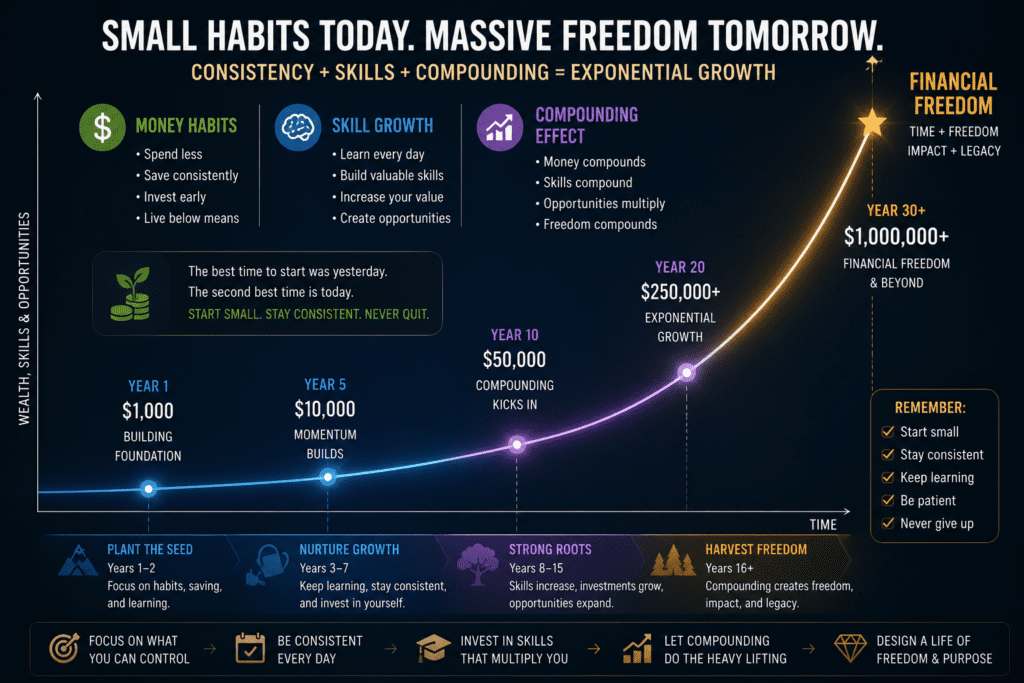

Rule 5: Compounding Is Slow Until It Becomes Fast

Compounding is one of those words everyone uses, but few people emotionally understand.

Compounding means small things grow when repeated consistently over time.

Money compounds. Skills compound. Trust compounds. Reputation compounds. Bad habits also compound.

If you save a small amount consistently, invest wisely, and avoid destroying your progress with bad decisions, the growth looks slow at first.

Then one day, it starts looking powerful.

The Investor.gov compound interest calculator is a useful tool to understand how money can grow over time with regular contributions and returns.

Compounding Is Not Only Investing

When I worked in electrical and plumbing work, every job taught me something. Then AC repair added another layer. Trading added psychology. Business added customers and marketing.

At the time, these things felt disconnected.

But later, they compounded.

Now when I write content, talk about trading psychology, explain business ideas, or discuss personal finance, all those experiences become useful.

Your life experience can compound if you reflect on it instead of running from it.

Small Compounding Habits

- Save a fixed percentage from every income

- Read 10 pages daily

- Track expenses weekly

- Improve one income skill every month

- Review trading mistakes instead of hiding from them

- Build one useful relationship per week

These habits look small.

But small habits repeated for years become a different life.

Rule 6: Use Hidden Opportunities Like Scholarships and Community Work

This is something many rich families understand earlier than others.

They don’t only think about money. They think about profiles, access, networks, and opportunities.

For example, many people think international scholarships are only about marks. Marks matter, yes. But in many cases, leadership, community service, volunteering, sports, projects, and meaningful activities can strengthen a student’s profile.

Some wealthy families guide their children early toward NGOs, charity foundations, sports, competitions, or community service.

Not always because they are “nice people” only. Sometimes they understand leverage.

Those experiences can open doors.

The Federal Student Aid website explains that scholarships can be based on different factors, including academic merit, talent, specific interests, or other criteria.

Here’s the lesson:

Opportunities are not always cash. Sometimes opportunity is a profile, a certificate, a relationship, a skill, or proof that you can lead.

How Beginners Can Use This

If you are young and don’t have money, don’t just complain that rich people have advantages.

Start building invisible assets:

- Volunteer in real community projects

- Join competitions or skill-based events

- Build a public portfolio online

- Learn freelancing skills and document results

- Create content around your learning journey

- Network with people in your field

- Apply for scholarships, grants, and financial aid

I wish I understood this earlier.

When you don’t have money, your proof of work becomes your currency.

My 7-Step Personal Finance System for Beginners

If I had to start again from zero, this is the system I would follow.

No fancy theory. Just practical steps.

Step 1: Know Your Monthly Survival Number

Write down the minimum amount you need to survive each month.

Include rent, food, transport, utilities, family obligations, and basic phone/internet.

This number tells you your financial baseline.

Step 2: Track Every Expense for 30 Days

For one month, track every rupee, dollar, or riyal.

Don’t try to change anything at first. Just observe.

Remember the mosquito example. Turn on the light first.

Step 3: Build a Small Emergency Fund

Start with one week of expenses.

Then one month.

Then slowly aim for 3-6 months.

Don’t feel ashamed if you start small. Starting small is still starting.

Step 4: Kill Bad Debt First

Bad debt is debt that does not increase income, skill, or productive value.

High-interest loans, emotional borrowing, luxury installments, and credit card debt can silently eat your future.

Pay those aggressively before trying to look like an investor.

Step 5: Build One Income Skill

Personal finance becomes easier when income grows.

But income should grow through skill, not gambling.

Choose one:

- Sales

- Copywriting

- Video editing

- Web design

- Trading education with strict risk control

- Digital marketing

- Technical repair skill

- Freelancing service

My electrician, plumbing, AC repair, trading, and business experiences all became part of my income skill stack.

Step 6: Invest in Assets and Knowledge

Once your foundation is stable, start learning investing properly.

Stocks, gold, silver, business, real estate, and digital assets all require understanding. Don’t enter because someone on social media posted profits.

Learn first. Risk small. Protect capital.

Step 7: Use Leverage Only After Proof

Don’t borrow money for an idea you have never tested.

Test small first.

If customers pay, if numbers make sense, if the process is repeatable, then leverage can help you scale.

Leverage before proof is gambling.

Leverage after proof can become growth.

Quick Action Steps

- Write your survival number today.

- Track every expense for the next 30 days.

- Cancel one unnecessary spending leak.

- Start a small emergency fund, even if it is tiny.

- Choose one income skill to build for the next 90 days.

- Before buying anything expensive, ask: asset or ego?

- Review your money every Sunday for 20 minutes.

Money Mistakes I Made and What I Learned

I don’t want to write this article like I was always financially disciplined.

I wasn’t.

I made mistakes. Real ones.

Mistake 1: I Thought Fast Money Would Solve Slow Problems

When I entered trading, I wanted quick results.

But trading punishes impatience. Funded accounts taught me that risk management is not optional.

Lesson: If your mindset is unstable, fast money systems can expose your weakness faster.

Mistake 2: I Ignored Mental Health Pressure

Family pressure and relatives’ words affected me deeply.

At times, I felt broken. I’m sharing this carefully because if someone reading this is in that dark place, please understand this:

Your life is more important than money, career, trading, business, or anyone’s opinion.

If you feel like harming yourself, talk to someone immediately — a trusted person, local emergency service, or mental health professional. The World Health Organization has resources explaining mental health and why support matters.

Lesson: Financial growth is important, but mental survival comes first.

Mistake 3: I Confused Activity With Progress

I was doing many things — work, trading, business ideas, learning — but sometimes without a clear system.

Busy does not mean productive.

Lesson: A simple money system beats random effort.

Mistake 4: I Wanted to Grow Before I Was Stable

This is common.

We want investment before emergency fund. Business expansion before customer proof. Leverage before cash flow.

Lesson: Stability first. Growth second. Leverage third.

Key Takeaways

- Personal finance rules are about awareness, control, security, and growth.

- The biggest money problem is often the one you cannot see.

- Rich people use leverage, but smart leverage comes after proof and planning.

- Middle-class money mistakes often come from trying to look rich too early.

- Emergency funds protect your decision-making and dignity.

- Compounding works in money, skills, trust, and reputation.

- Scholarships, community service, and proof of work are hidden financial opportunities.

- Before using debt or investor money, test your idea small.

- Financial growth without mental health is not real success.

“Do not save what is left after spending, but spend what is left after saving.”

— Warren Buffett

“The goal of a successful trader is to make the best trades. Money is secondary.”

— Alexander Elder

Frequently Asked Questions

What are the most important personal finance rules for beginners?

The most important personal finance rules for beginners are: know your monthly survival number, track expenses, build an emergency fund, avoid bad debt, grow one income skill, invest in knowledge, and use leverage only after testing your idea or system.

How do rich people think differently about money?

Rich people usually think in terms of leverage, systems, assets, networks, and long-term value. Instead of only asking how much money they have, they ask how to use resources wisely to create more value without taking reckless risk.

Is leverage good or bad in personal finance?

Leverage can be good or bad depending on how it is used. Good leverage includes scholarships, useful tools, tested business funding, and partnerships. Bad leverage includes high-interest debt, luxury installments, and trading with high risk without discipline.

How much emergency fund should I have?

A good target is 3-6 months of basic living expenses, but beginners can start with one week or one month of expenses. The goal is to create financial breathing room so you do not make desperate money decisions.

Should I invest before paying off debt?

If you have high-interest bad debt, it is usually better to focus on paying it down before taking investment risk. Low-interest productive debt may be different, but beginners should prioritize stability, emergency savings, and debt control first.

Why do middle-class people struggle with money?

Many middle-class people struggle because they spend to look successful, ignore small money leaks, use debt emotionally, and focus more on income than systems. Without financial awareness, higher income can still disappear quickly.

Can I build wealth if I am starting from zero?

Yes, you can build wealth from zero, but it requires patience, awareness, income skill development, emergency savings, and consistent financial discipline. Start with proof of work, small savings, and one valuable skill before using leverage.

Final Thoughts: Personal Finance Rules Can Change Your Life

Look, I know personal finance can feel boring when you are under pressure.

When bills are waiting, family is taunting, income is low, and your mind is tired, budgeting feels small. Saving feels slow. Tracking expenses feels annoying.

But here is what I learned from my own journey:

The person who becomes financially aware becomes harder to control.

Once you know your numbers, you stop guessing. Once you stop spending to impress people, you keep more money. Once you build skills, you increase income. Once you protect capital, you survive longer. Once you understand leverage, you stop thinking like a victim.

These personal finance rules are not magic.

They are simple. But simple does not mean easy.

Start with awareness. Turn on the light. Find the mosquito. Then fight.

If this article helped you, share it with someone who is trying to build their life from zero. And if you are serious, open your notebook today and write your survival number.

That one number can be the beginning of your financial comeback.

About the Author

Shurah Beel Hamid is a business enthusiast, active trader, and content creator focused on business strategies, Forex and gold trading, compounding, freelancing, trading psychology, elite mindset, self-improvement, and personal finance.

His writing is based on real experience — from working as an electrician, plumber, and AC repair worker to trading, building small business ideas, moving abroad, and learning money lessons the hard way. Shurah shares practical advice for people who want to grow financially and mentally from the ground up.

Disclaimer

This article is for educational and personal experience purposes only. It is not financial, investment, trading, legal, tax, or mental health advice. Trading forex, gold, stocks, funded accounts, or any financial market involves risk and can result in loss of capital. Always do your own research and consult qualified professionals before making financial decisions.

If you are struggling with thoughts of self-harm or extreme mental stress, please contact local emergency services, a trusted person, or a qualified mental health professional immediately. Your life matters more than any financial goal.